Treasuries / Agencies

- Treasury yields rallied approximately 100 to 110 basis points from their peak in October and we look for a slight back up early 2024.

- Political and geopolitical risks could keep volatility elevated.

- We believe the market is too aggressive with the timing and amount of interest rate cuts.

- Given the Federal Reserve’s aggressive hiking campaign is likely over, we favor adding duration opportunistically and a bulleted yield curve posture.

ABS

- We see trust performance metrics are still trending down.

- Muted new issuance volume in the fourth quarter of 2023.

- We continue to prefer liquid, defensive tranches from credit card, prime auto and equipment deals.

CMBS

- CMBS delinquencies continue to worsen, with worrying trends in the multifamily subsector.

- We believe the move lower in rates helps loan refinancing on the margin but is not a panacea for troubled office properties.

- We continue to favor more stable non-agency conduit tranches and agency CMBS but are mindful of recent spread tightening

RMBS

- Mortgage returns were healthy in the fourth quarter.

- Despite the recent drop-in mortgage rates, prepayment speeds are unlikely to accelerate significantly.

- We find value in non-agency single family rental (SFR) as housing market dynamics are supportive.

Municipals

- Municipal issuer credit fundamentals continue to be healthy in our view.

- State and local issuers have implemented budget adjustments to adjust for lower revenue growth.

- Healthcare systems are experiencing a rebound in operating margins.

- We view an allocation to the municipal sector as a defensive alternative to other spread sectors.

Investment Grade Credit

Recap: The fourth quarter saw the investment grade credit market make a sharp turn in following up a challenging October with two very strong months of performance on a total and absolute return basis in November and December to close out the year as Treasury yields collapsed over the quarter. The quarter kicked off in disappointing fashion with another month of negative excess returns given 10 basis points of widening in the option-adjusted spread (OAS) of our bellwether front-end corporate credit index, the ICE BofA 1-5 Year U.S. Corporate Index, in October, marking the third consecutive month of spread widening. Markets were rocked in October by the flareup in tensions in the Middle East and potential follow-on impact on energy markets as well as further concerns central banks may maintain higher policy rates for longer, which weighed on risk assets. The corporate bond market reversed course in November and had its best month since the snapback seen the prior November. Both total and excess returns were very strong, helped by the sharp drop in Treasury yields, growing belief the Federal Reserve was done hiking, and benign economic growth outlook being priced in among the key factors. Markets were buoyed by generally favorable news on the inflation front as market hopes grew for a soft landing and central bank policy rate cuts began to be priced in for the first half of 2024. In December the corporate bond market maintained some of its momentum from November in posting another solid month of relative performance despite another sharp drop in Treasury yields. The strength in total and excess returns was bolstered by what the market interpreted as a bona fide dovish pivot by Chair Powell and the Federal Reserve in signaling at the December FOMC meeting its hiking cycle was done while a soft landing definitively became the overwhelming market consensus.

Shifting briefly to fundamentals, third-quarter earnings reports, which printed throughout the fourth quarter, ended the multi-quarter string of negative year-over-year earnings comparisons with a mid-single-digit growth print for S&P 500 Index companies. However, as tracked by JP Morgan, in terms of other credit and related metrics, gross debt leverage continued to tick higher, revenue growth turned slightly negative, operating income as gauged by EBITDA declined, and interest expense coverage dropped. We will get a further insight into corporate performance with the upcoming quarterly earnings season about to kick off in early January.

Portfolio Actions: Given our more cautious market outlook and less than bullish view on the direction of credit spreads entering the fourth quarter, we were a bit wary about dialing up our risk positioning or looking to add exposure to the investment grade corporate bond sector. Over the fourth quarter in the Cash Plus strategy we replaced maturities mainly with selected purchases of six-month to one-year duration area secondary bonds at what we deemed attractive yields. It was a similar story in the Enhanced Cash strategy where we maintained our sector weighting by locking in attractive yields by adding 6-9-month maturity secondary bonds. In the 1–3-year strategy portfolios, we selectively added primarily one-year and shorter duration secondary bonds in a few of our favored subsectors, maintaining overall sector exposure Those purchases were funded by selling roughly half-year or shorter duration bonds. In the 1–5-year strategy portfolios, where we also kept our sector weighting relatively constant over the quarter, we carried out an extension trade in a U.S. utility holding company out of a one-year bond into a three-year new issue as well as added a U.S. money center institution’s bank-level three-year new issue. We also sold a pharmaceutical company’s new three-year issue bond that came to market in May, whose spread had tightened post issuance to fund our sector buys.

Outlook: Coupling the steady erosion in corporate credit fundamentals we are witnessing with the robust excess returns in the investment grade corporate bond market realized in the fourth quarter driven by meaningful spread compression in the last two months of the year, we believe the outlook over coming quarters is less sanguine. We continue to maintain that we are in a “late�cycle” environment that has been extended or a more pronounced decline in economic growth delayed in the aftermath of the record amount of pandemic-era stimulus for companies and consumers, a record amount of surplus cash accumulated, and sustained benefit of zero interest rates. We have already seen corporate defaults and distressed exchange activity increase as lending conditions have tightened coupled with rising consumer stress via higher delinquency rates. Thus, despite the market pricing in a rather benign end to the Federal Reserve’s hiking program or “soft landing”, we anticipate the landscape, especially as it relates to corporate credit, could be more challenging in 2024.

The substantial move higher in risk assets in the fourth quarter, as seen in the nine-week winning streak of the S&P 500 Index to close the year, pushed credit spreads to levels that fail to adequately price in some of the risks we see materializing. The upcoming year faces major challenges in terms in whether the U.S. economy will be able to skirt a recession, potential tightening in financial conditions, heightened geopolitical uncertainties including China-U.S. relations, the Ukraine-Russia standoff, the situation in the Middle East, and the divided U.S. political landscape which will be in the spotlight in the runup to the presidential election. This year we could also see the U.S. lose its Moody’s Aaa rating, assigned a negative outlook in November, an event that could spark market volatility given this represents its lone remaining major rating agency AAA rating. Overall, we anticipate that we will see spread widening given growing headwinds and are positioned for a likely reset wider in credit spreads. We think the Federal Reserve may be more patient than the market forecasts in terms of initiating rate cuts later in the year, as inflation may prove stickier to the upside than is anticipated keeping the Fed in a “higher-for-longer” mode. We remain very selective in the investment grade credit sector and maintain a lesser risk positioning than our norms across strategies representing a lower sector weighting and more defensive, up�in-quality positioning. We favor more generally less cyclically exposed subsectors like Banking, Insurance, Communications, Consumer Non-cyclicals, and Electric Utilities, better protected against spread widening in our view

Performance: The investment grade credit sector contributed positively to relative performance across all strategies in the fourth quarter. Positive excess returns from the sector were driven by the overall tightening in credit spreads we witnessed. Corporates benefited from the steep drop in Treasury yields, growing belief the Federal Reserve is done hiking, and benign economic growth outlook being priced in among the key factors.

After the large increase in benchmark Treasury yields in October, markets shifted with interest rates declining significantly in the last two months of the year. Although credit spreads typically move in the opposite direction of yields, the fall in yields and more benign consensus outlook drove investors to aggressively push spreads lower, producing some of the highest two-month all-in total returns the markets have seen. The OAS of our front-end benchmark ICE BofA 1-5 Year U.S. Corporate Index tightened 18 basis points on a quarter-over-quarter basis to a level well below where we began the year. With the meaningful credit spread tightening and decrease in benchmark yields, the index’s fourth-quarter total return and excess return were 3.96% and 0.85%, respectively. Strongly performing investment grade credit subsectors that drove positive excess returns across strategies included Banking, Insurance, Automotive, Wireless, Midstream and Electric Utilities.

Treasuries / Agencies

Recap: The Treasury market staged a massive rally in the fourth quarter as the markets read the Fed’s December Summary of Economic Projections (SEP) and Chair Powell’s post-meeting press conference as dovish. In the subsequent days, several Fed members attempted to push back on the dovishness by rebuffing the market timing of the first cut, but the effort fell on deaf ears as the market is still pricing in a greater than 65% chance of a rate cut in March.

In December the FOMC unanimously voted to hold interest rates steady for a third straight meeting, with the Fed last hiking rates by 25 basis points to a target range of 5.25%-5.50% in July and skipping their next three meetings in September, November and December. The FOMC dots released at the December meeting projected a series of three quarter-point cuts in 2024 to 4.625%, which helped provide a clear signal that its aggressive hiking campaign was over. According to the median estimate the FOMC also projected further reductions in the federal-funds rate by the end of 2025 to 3.625%. The FOMC statement was tweaked by adding one word to the statement, with the committee monitoring developments to see if “any” additional policy firming is appropriate. Powell said the committee discussed rate cuts at the meeting but hasn’t ruled out the possibility of another hike if the data calls for it, adding to the sense of a dovish pivot. It was a strong signal that the FOMC is not looking to raise rates anytime soon which was an important acknowledgement. The market embraced the more dovish tone from the FOMC as the two-year Treasury saw its largest rally since March during the fleeting regional banking crisis, as the yield moved 30 basis points lower to 4.43% from 4.73% on December 12. To put this into perspective, you would have to go back to 2008 for similar moves.

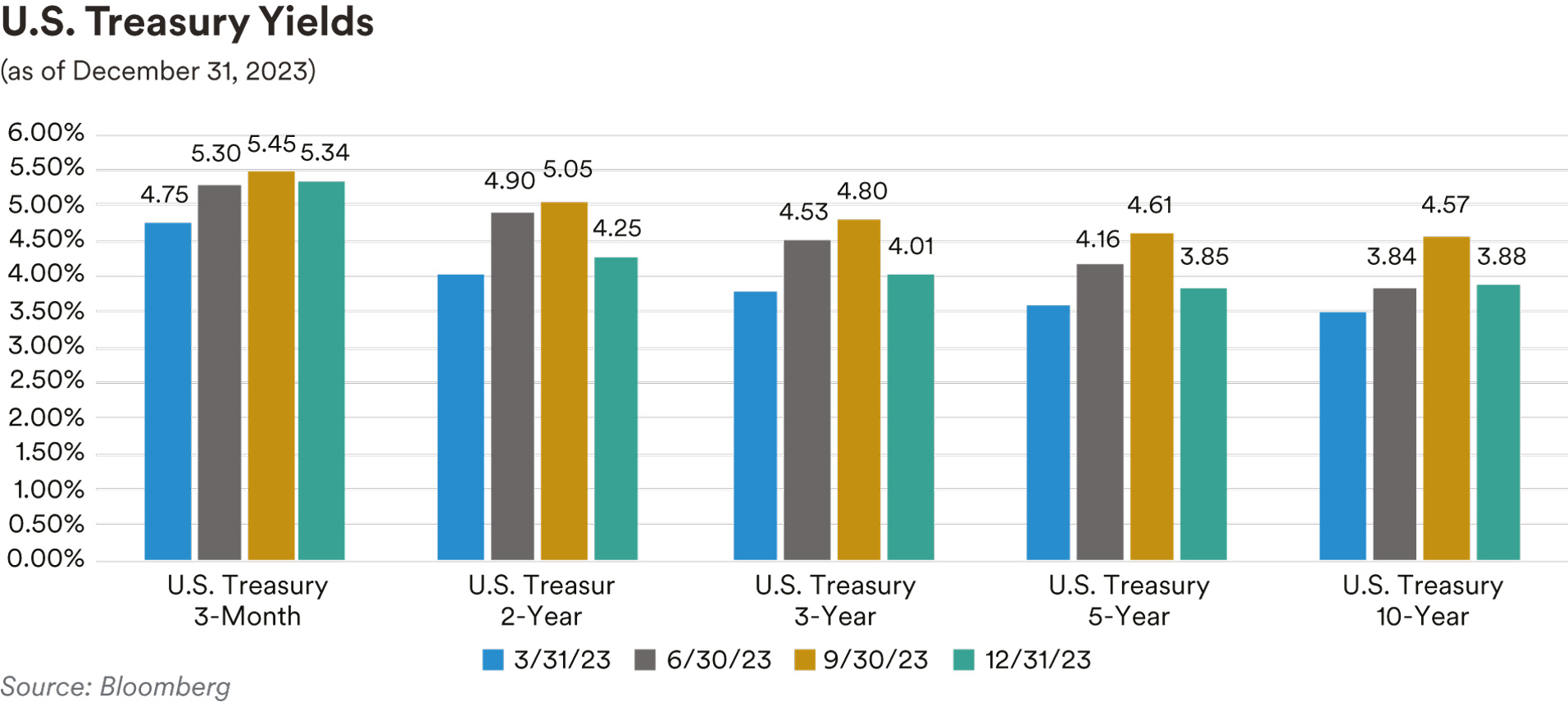

In the very front end of the market where we operate, short Treasury bill rates rallied less than further out curve over the fourth quarter. The three-month, six-month, and one-year bill yields were 12, 29 and 69 basis points lower during the quarter, respectively. The two-year Treasury moved 79 basis points lower, ending the quarter at 4.25%. The five-year Treasury rallied by 76 basis points and ended the quarter at 3.85% while the ten-year Treasury moved 69 basis points lower to end the quarter at 3.88%. The spread between the 10-year Treasury and the 2-year Treasury steepened from -47 basis points at the start of the quarter to -37 basis points at the end of the quarter. The spread between the 5-year Treasury and 2-year Treasury moved marginally steeper from -43 basis points at the start of the quarter to -40 basis points at the end of the quarter.

When the Treasury released its quarterly refunding announcement, it pointed to the strong demand for Treasury bills, rising term premium and higher bill issuance vs. coupons to help fund the growing fiscal deficit. We saw an ongoing decline in RRP (reverse repo program) usage, the largest participants of the program being money market funds continuing to reallocate capital from the RRP into the Treasury bill market.

Treasury Inflation-Protected Securities (TIPS) breakeven inflation rates moved lower during the quarter. The five-year real yield moved from 240 basis points at the start of the quarter to 187 basis points at the end of the quarter. The ten-year real yield went from 223 basis points to 171 basis points during the same period. Five-year TIPS breakeven rates moved lower to 215 basis points from 225 basis points at the start of the quarter while ten-year TIPS declined to 217 basis points from 234 basis points over the same period. During the quarter, we saw five and ten-year breakeven rates peak in mid-October at 246 and 249 basis points, respectively.

-breakeven.jpg)

Front-end Government-Sponsored Enterprise (GSE) agency spreads tightened in sympathy with credit spreads over the fourth quarter as the OAS of the ICE BofA 1-5 Year U.S. Bullet (fixed maturity) Agency Index ended the quarter at just 1 basis point, 7 basis points tighter from the start of the quarter. In the SSA (Sovereigns, Supranationals & Agencies) subsector, U.S. dollar�denominated fixed-maturity security spreads were marginally tighter by 2 basis points and finished the quarter on average at 27 basis points over comparable-maturity Treasuries. Agency callable spreads relative to Treasuries widened as short-dated and short-expiry volatility in the upper left portion of the volatility surface moved higher over the quarter. Two- and three-year maturity “Bermudan” callables, which feature quarterly calls with lockout periods of three months, saw spreads over Treasuries widen from 75 and 120 basis points from the start of the quarter to 110 and 140 basis points at the end of the quarter, respectively.

Portfolio Actions: In the fourth quarter, we slightly decreased our allocation to Treasuries in favor of high-quality spread sector alternatives. We continued swapping shorter-term Treasuries to extend our portfolio durations using Treasuries and various high-quality securities further out the curve. As five- and ten-year TIPS breakevens fell to 216 and 217 basis points respectively, we took the opportunity to add TIPS across our 1-3 and 1-5-year strategy portfolios late in the quarter. Having last held TIPS in our portfolios in January 2021, we purchased TIPS as we believe inflation will remain sticky in the first half of 2024 and a dovish Fed should be supportive of higher breakevens than current levels. As the yield curve steepened during the quarter, we continued to “bullet” up our yield curve posture while adding duration across our strategies. Portfolios in our 1-3-year strategy had a slight barbell positioning as the five-year TIPS position possesses key rate durations weighted in the five-year part of the curve, which is outside of the respective benchmarks.

Outlook: As we start the new year, we think the market’s enthusiasm around the Fed hitting its 2% inflation target, coupled with hopes over the amount and timing of aggressive interest rate cuts we saw the market price in in November and December could prove overly optimistic. Some of the risks to which we remain attuned that could impact markets this year center on the U.S. political backdrop, geopolitics and the stickiness or upward pressure on inflation due to solid wages, shelter, and the increasing shipping-related supply chain costs. The attacks on commercial shipping vessels in the Red Sea by the Iran-linked Houthi rebels have sent shipping costs surging. We think the Red Sea crisis could lead to disruption in the supply chain and cause consumer price increases. Just in the first week of the new year, the World Container Index, which tracks global container rates, has spiked to its highest level since November 2022. As a result, we could see the price of oil spike and with 15% of the world’s shipping traffic passing through the Suez Canal each year, there is a real risk that the path of inflation could reverse course. We expect the Treasury to lean on front-end issuance for supply needs and will look for additional clues in their next refunding announcement due at the end of January. We will be watching technical support levels for two�year Treasury rates at 4.45% and five-year Treasury rates around 4.10% to opportunistically look to add duration to our portfolios.

As for Quantitative Tightening (QT), the FOMC’s December meeting minutes showed they felt the runoff of the Fed’s bond portfolio has “proceeded smoothly” so far. This represented the first public discussion about the end of QT. A recent speech by Dallas Fed President Logan suggests she was one of the “several” participants suggesting a conversation on when it will be appropriate to slow the pace of QT “well before such a decision was reached”. We think this was prompted by pressure in the repo markets seen near the end of the year. Logan linked the QT slowdown to overnight RRP levels as she stated, “in my view, we should slow the pace of runoff as overnight RRP balances approach a low level”. Although she did not go on to elaborate on what this low level is, currently the RRP balance is around $700 billion, while market consensus regarding this “low level” is around $200-250 billion, which could be reached sometime in the second quarter given the pace of reductions in RRP since September.

We expect agency callable redemptions to rise in 2024 due to the significant amount of callables maturing and those eligible to be called with the anticipation of lower rates. We estimate $415 billion of redemptions among the $660 billion of callable bonds that are up for call this year. We believe the current level of volatility will remain elevated for some time and think callables continue to look attractive given their wide spreads to Treasuries. As such, we will look for opportunities to add positions to our portfolios. We anticipate GSE and SSA spreads to continue to trade in their current range early in 2024 with a slight bias to move marginally wider due to heavier issuance in the first half of the year as SSA issuers tend to front-load their supply needs.

Performance: Our slight short duration posture at year end was a detractor from excess returns across all our strategies as rates rallied over the quarter. Our curve positioning in our Cash Plus and Enhanced Cash strategies were additive to performance while it generated negative performance in our 1-3 and 1-5-year portfolios. The agency sector saw positive excess returns across all our strategies which hold mainly agency callables.

ABS

Recap: With the exception of subprime auto tranches, short-tenor ABS spreads generally moved tighter over the fourth quarter as the market found support from lower interest rates, a relatively firm labor market, and the perception that that Fed was at the end of their tightening cycle. Concerns about a possible economic slowdown remain but any anticipated downturn is now expected to occur later, possibly in the second half of 2024. Benchmark three-year, AAA-rated credit card and prime auto tranches ended the quarter at spreads of 51 and 63 basis points over Treasuries, 4 and 17 basis points tighter, respectively according to street research. Three-year, floating-rate AAA-rate private student loan tranches ended the quarter at a spread of 126 basis points over SOFR, 6 basis points tighter. In contrast, subprime autos were slightly weaker over the quarter with benchmark three�year, AAA-rated tranches ending the quarter at a spread of 93 basis points over Treasuries, 3 basis points wider. We attribute the underperformance of subprime auto tranches to investors preference for more liquid, higher quality collateral. For the year, benchmark three-year, AAA-rated credit card, prime and subprime auto tranches were 5 basis points wider, 23 basis points tighter and 24 basis points tighter, respectively. We attribute the relative underperformance of credit card tranches to a modest reversal from the dramatic rally in credit card spreads seen in December last year (spreads moved 26 basis points tighter in December 2022 to end the year at 46 basis points over Treasuries). Broadly syndicated loan (“BSL”) CLOs ended the year at a spread of 143 basis points over SOFR, 57 basis points tighter on the year. Fourth-quarter ABS new issue volume was muted with just $54 billion of new deals coming to the market, a 24% drop compared to the $71 billion seen in the third quarter but still up 14% relative to the fourth quarter last year which saw $47 billion of new issue deals. As usual, the auto subsector was the largest contributor to new supply, with over $33 billion of new deals coming to market. This was followed by over $7 billion of issuance in the “other ABS” subsector (a “catch-all” category which includes deals collateralized by cell phone payment plans, timeshares, mortgage servicer advances, insurance premiums, aircraft leases, etc.) and $4.5 billion of new credit card issuance. For the year, ABS new issuance totaled $256 billion in 2023 of which 56% came as Rule 144A and 7% as floating rate. In comparison, 2022 new issuance totaled $244 billion with 50% coming as 144a and 4% issued as floating rate.

Credit card trust performance metrics continued to show signs of deterioration over the fourth quarter. Data from the JP Morgan credit card performance indices reflecting the December remittance reporting period showed charge-offs and 60+-day delinquencies on bank credit card master trusts rising 15 basis points and 12 basis points, respectively, over the quarter, to 2.00% and 1.00%. However, despite this increase, charge-offs and delinquencies remain well below historical norms. We expect to see continued deterioration in credit card performance metrics going forward as rising unemployment, dwindling savings, higher interest rates and persistent inflation impact consumers. However, as we have noted in previous commentaries, despite the possible headwinds we do not anticipate a material impact on our credit card holdings due to their robust levels of credit enhancement. In addition, we believe that ABS credit card trusts are likely to perform better than broader credit card portfolios due to their significantly more seasoned accounts. For example, the Fed reports that the charge-off rate for commercial bank credit card loans was 3.49% in the third quarter, compared to 1.85% for bank credit card master trusts. At the end of the year, bank credit card master trust balances stood at $13.7 billion, $1.2 billion higher than at the end of 2022.

New vehicle sales numbers in December came in above expectations to end the year at a 15.8 million SAAR (seasonally adjusted annualized rate) pace, following a dip in November to 15.3 million SAAR. For the year, sales have been rangebound between 14.8 and 15.8 million SAAR, after ending 2022 at 13.3 million SAAR. As we noted in last quarter’s commentary, higher interest rates and rising auto prices are the current constraints on new vehicle sales in contrast to the limited inventory of vehicles seen in 2022 (a consequence of the computer chip shortage and supply chain bottlenecks). The UAW strike, which ended in late October, does not seem to have materially impacted sales volumes. In our view, this was likely due to the “Stand Up” strike tactic employed by the UAW (targeting specific plants rather than a more broad-based strike), which minimized the strike’s impact on new vehicle production. Cox Automotive estimated that at the start of December the new vehicle inventory stood at 2.56 million units, 900,000 higher year-over-year. This level reflected 71 days of supply, 17 days greater than in December 2022. Cox noted that large year-over-year gains were delivered by Honda, Nissan, General Motors and Tesla. Hyundai also had a strong year, growing sales by more than 12% and surpassing Stellantis – maker of Jeep, Ram, Dodge, Chrysler and other brands – to take the fourth spot in overall U.S. sales, behind GM, Toyota and Ford. After treading water during the third quarter, used car prices, as measured by the Manheim Used Vehicle Index, dropped significantly over the fourth quarter, ending 2023 at 204.0, a low for the year and down 7% from a year ago. This year’s drop in used car prices follows the 15% decline seen last year. Manheim noted that all major market segments saw year-over-year price declines. Luxury vehicles, pickups and SUVs performed better than the overall market (down 6.9%, 6.5% and 6.1%, respectively). Compact cars were the worst performers (down 11.7%), followed by midsized cars (down 8.1%) and vans (down 7.9%).

Falling used vehicle prices are a notable headwind for auto ABS trust performance. As of November’s data, the 60+-day delinquency rates on the Fitch Auto ABS indices were 0.28% for the prime index and 5.88% for the subprime index, numbers which reflect increases of 5 basis points and 67 basis points, respectively, from last year’s levels. Likewise, annualized net loss rates for the indices stand at 0.43% for the prime index and 10.05% for the subprime index, 13 basis points, and 202 basis points higher, year-over-year, respectively. As we noted in our third quarter commentary, we believe the divergence between prime and subprime performance can be attributed to the fact that prime borrowers are better positioned than subprime borrowers to weather the impact of rising interest rates and the pressures of higher prices. Despite the continued erosion in auto ABS trust performance metrics, we remain comfortable with our holdings in AAA and AA-rated auto tranches as in our view these deals have sufficient credit enhancement to protect bondholders. However, as we noted in our third quarter commentary, we generally prefer adding prime tranches to the portfolios rather than subprime tranches at current spread levels.

The most recent Fed Senior Loan Officer Opinion Survey, reflecting sentiment as of October, showed a significant net share of banks reporting tightening lending standards for credit cards and other consumer loans. A moderate net share of banks also reported tightening auto loan standards. A significant share of banks reported weaker demand for auto and other consumer loans, while a modest net share of banks reported weaker demand for credit card loans. The survey included a set of special questions that asked banks to evaluate the likelihood of approving credit card and auto loan applications by borrower FICO score compared to the beginning of the year. A significant share of banks reported they were less likely to approve both for borrowers with FICO scores of 620 and a moderate and significant share of banks reported they were less likely to approve credit card and auto loan applications, respectively, for borrowers with FICO scores of 680. In contrast, a modest net share of banks reported they were more likely to approve credit card applications to borrowers with FICO scores of 720, while the likelihood of approving auto loan applications to such borrowers was unchanged. In our view, these responses validate our outlook that lower income consumers face greater challenges from rising rates, inflation and a slowing economy than higher-income consumers.

Portfolio Actions: Continuing our strategy from the third quarter, we increased portfolio exposure to ABS across most of our strategies during the fourth quarter. The short duration profile of liquid ABS tranches is a more natural fit for our shorter strategy portfolios. Notably, the degree of increase was more pronounced in our shorter Cash Plus and Enhanced Cash strategies compared to our 1-3-year and 1-5-year strategies. We continued to favor adding to our credit card and prime auto holdings in order to bolster the liquidity profile of the portfolios rather than reaching for incremental yield in subprime auto and more esoteric subsectors. As in the third quarter, we continued to purchase the front-pay “CP” tranches of various auto and equipment deals in our shorter strategies (these tranches stand at the top of the payment waterfall and carry short�term commercial paper ratings equivalent to AAA. Since they are structured to receive the first principal payments from these deals, they are the safest tranches in ABS deal structures from a credit perspective.) In our longer portfolios we focused on 1-year and 2-year AAA-rated senior tranches. These securities have a favorable liquidity profile due to their very short average lives and continue to benefit from the inverted yield curve, so they often provide higher yields than longer tenor alternatives. Our purchases occurred in both the primary new issue and secondary markets. Within the Other ABS subsector, we added exposure to rental fleet ABS via secondary market purchases. We met with representatives of several auto rental companies at the ABS East conference in October and evaluated their issuance programs. In our opinion, the exit of one such issuer from bankruptcy in 2021 served to validate performance of the subsector and we found the incremental spread of these AAA-rated tranches attractive relative to benchmark auto and fleet lease alternatives.

Outlook: Our outlook for ABS remains essentially unchanged. We anticipate worsening economic conditions going forward that will negatively impact ABS trust performance. Accordingly, we are likely to continue to target our purchases toward more defensive tranches and subsectors. We still favor short-tenor auto and equipment tranches but are mindful of the recent spread tightening in these subsectors. As noted above, we prefer prime auto over subprime. That said, we remain comfortable with a select group of subprime issuers who have a demonstrated history of successfully operating through credit cycles and who have business models and underwriting practices with which we are very familiar. We continue to avoid increasing our CLO exposure as we believe leveraged loans will suffer heightened downgrades and defaults which would bias CLO spreads to moving wider.

Performance: Our ABS positions produced positive results across all of our strategies in the fourth quarter, with notable outperformance in our Enhanced Cash, 1-3 year and 1–5-year strategies. All subsectors were generally positive with our fixed-rate auto tranches performing best and our fixed-rate fleet lease tranches also performing very well. Our private student loan holdings were generally the laggards with flat performance across most strategies. As in prior quarters, our CLO holdings were very slightly positive for the quarter.

CMBS

Recap: After moving wider in October, spreads on short-tenor CMBS tranches recovered and ended the fourth quarter tighter as muted new-issue supply offset persistent negative headlines emanating from the office subsector. At the end of the quarter, spreads on three-year AAA-rated conduit tranches stood at 128 basis points over Treasuries, 8 basis points tighter than at the start of the quarter. Spreads on five-year AAA-rated conduit tranches were 140 basis points over Treasuries, 5 basis points tighter. Three-year Freddie Mac “K-bond” agency CMBS tranches ended the quarter at a spread of 28 basis points over Treasuries, 8 basis points tighter. For the year, spreads ended slightly wider with three and five-year conduit tranches 3 basis points and 12 basis points wider and three-year “K-bond” tranches 1 basis point wider, respectively. Three-year, AAA-rated, floating-rate single-asset, single-borrower (“SASB”) tranches ended the year at a spread of 148 basis points over SOFR, 32 basis points tighter. Issuance volume declined relative to the last quarter with only $44.8 billion in new deals coming to market, compared to over $50.3 billion in the third quarter. Issuance continues to be dominated by the agency sector with almost $29.0 billion of agency deals printing, in comparison to only $15.9 billion of non-agency deals. While the quarter’s non-agency volume was essentially flat to last quarter and low relative to agencies, it roughly equaled the combined total of first and second quarter non-agency new issuance. For the year, CMBS issuance totaled $170.2 billion, a decline of over 34% relative to the $258.4 billion issued in 2022. Non-agencies bore the brunt of the year-over-year decline, with issuance down 55% to $47.7 billion in 2023 from $105.6 billion in 2022. Agency new issuance dropped 20% to $122.5 billion in 2023 from $152.8 billion last year. Going forward, we anticipate a modest recovery in non-agency issuance in 2024 as the recent move lower in interest rates should support refinancing activity on the margin.

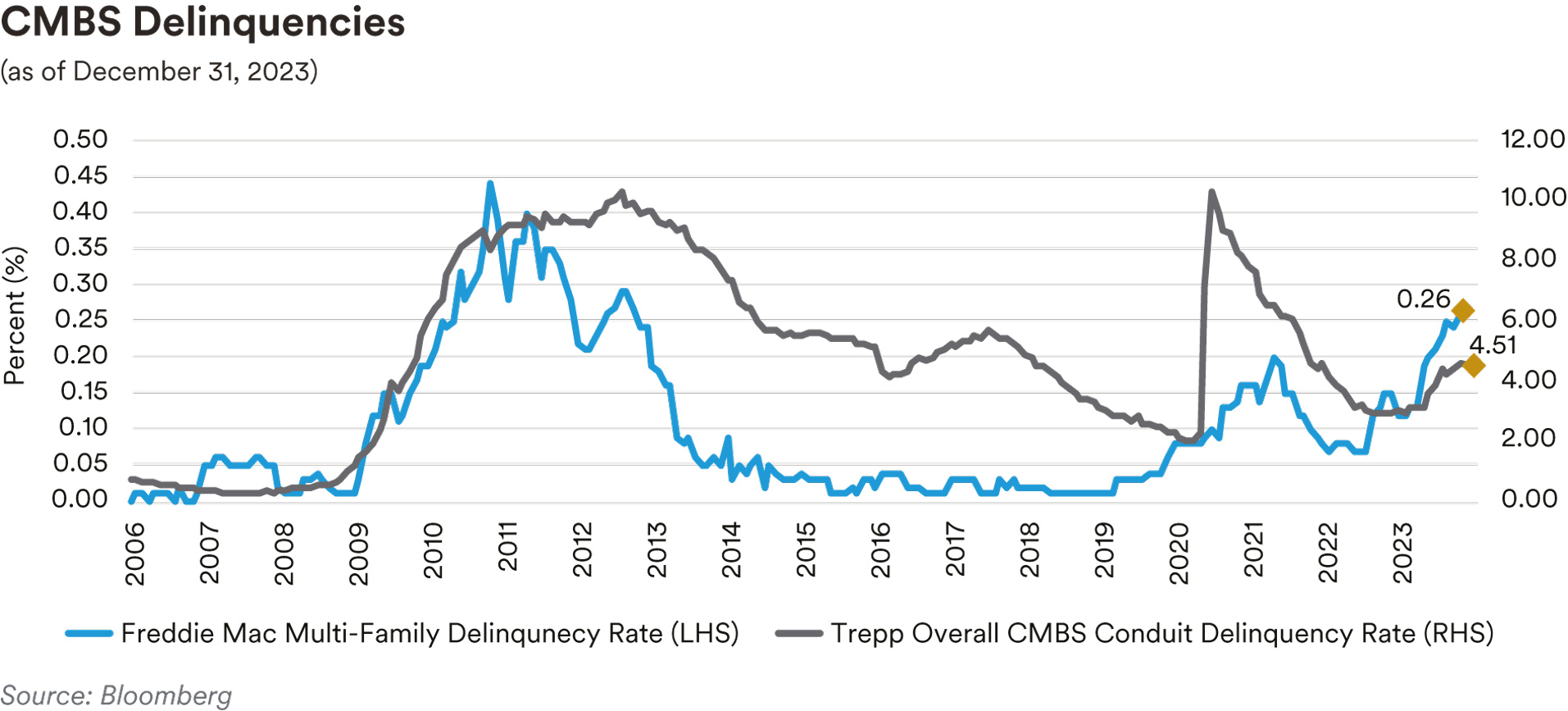

Despite a modest improvement in December, CMBS delinquencies ended the quarter higher with weakness in multi-family properties being a notable contributor. As measured by the Trepp 30+- day delinquency rate, CMBS delinquencies ended the year at 4.51%, an increase of 12 basis points for the quarter and 147 basis points for the year. The all-time high on the delinquency rate was 10.34%, registered in July 2012 and the more recent COVID-19 high was 10.32%, seen in June 2020. December saw a modest improvement in delinquencies (falling 7 basis points) and Trepp noted that the heavily watched office segment saw lower delinquencies for the first time in several months. Office delinquencies fell 26 basis points in December to 5.82%, but despite this recent improvement still ended the quarter 24 basis points higher. Multifamily delinquencies rose 16 basis points in December and were the worst performing subsector over the quarter with delinquencies rising 77 basis points. Retail properties were the best performing over the quarter with delinquencies dropping 45 basis points to 6.47%. Despite recent improvement, retail remains the worst performing subsector overall. Industrial properties remain the best performing, with delinquencies ending the year at 0.57%, 27 basis points higher over the quarter and 15 basis points higher for the year.

Commercial property prices continue to fall, although the pace of the decline seems to be easing. The December release of the RCA CPPI National All-Property Composite Index showed prices have fallen 8.0% year-over-year through November to 146.4, not surprisingly, given all the negative headlines and sentiment, office properties posted the largest annual decline, with prices falling 14.9% year-over-year. Weakness in office properties, driven by the dynamic of remote work and the shock of higher rates, has been led by central business district (“CBD”) offices which saw prices drop 26.0% for the year, while suburban office prices fell 12.4%. Apartment properties were the next worst performing with prices falling 2.1% over the quarter and 12.1% year-over-year. Industrial properties were the only subsector to show a gain with prices up 2.7% over the quarter and 1.8% year-over-year despite taking a dip around midyear.

The current Fed Senior Loan Officer Opinion Survey showed a significant net share of banks reported tighter lending standards and weaker demand for all types of commercial real estate loans.

Portfolio Actions: During the quarter we modestly increased our CMBS exposure across our strategies. As we have noted in prior commentaries, we have favored short-tenor investments in both agency CMBS and more stable conduit ASB tranches. We added both types of investments over the course of the fourth quarter, accounting for the increase in CMBS exposure. Our activity consisted of secondary market purchases as we did not participate in any new issue deals during the quarter.

Outlook: As we enter 2024, our outlook for CMBS is relatively unchanged. We continue to be very cautious as we anticipate continued worsening delinquencies and falling commercial property prices. In particular, we are closely watching the deterioration in multifamily delinquencies which could have knock-on effects in the agency sector. Although the recent move lower in interest rates should help refinancings on the margin, we are not anticipating any dramatic improvement in fortunes for troubled office properties. While the coming year’s conduit refinancing volume (estimated to be about $34 billion) seems manageable, we are mindful that refinancing pipeline volume is greater than that for the upcoming five years before dropping markedly in 2030. In accordance with historical patterns, we expect a more bullish tone to the market post the early January Commercial Real Estate Finance Council (CREFC) conference in Miami, but we believe any improvement in market sentiment is unlikely to be long-lasting absent some meaningful improvement in the outlook for office collateral. As noted above, this is not something we anticipate in the near term.

Performance: Our CMBS positions posted positive performance across all of our strategies in the fourth quarter after adjusting for duration and yield curve positioning. In general, our non-agency positions were positive, with our AAA and AA-rated floating-rate SASB holdings the best performing of all our CMBS exposure. Our agency holdings were also positive with our Freddie Mac “K-bond” and Fannie Mae “DUS” holdings generally performing better than our Freddie Mac “Small Balance” CMBS positions. Across our strategies, the shorter Cash Plus and Enhanced Cash portfolios saw the greatest excess returns from CMBS. This was the result of their greater exposure to floating-rate SASB tranches relative to our longer strategies.

RMBS

Recap: Residential mortgage-backed securities posted positive performance over the course of the fourth quarter as spreads trended tighter after the third quarter’s lackluster results. Reminiscent of last year’s fourth quarter, November saw the highest returns for mortgages all year with the Bloomberg mortgage index posting a 1.33% monthly excess return (last year, November was also the best month for mortgages with a 1.35% excess return). This November, mortgages benefited from the rally in rates and reduced selling from REIT and bank portfolios. Overall, generic 30- year collateral ended the quarter at a spread of 137 basis points over ten-year Treasuries (38 basis points tighter) while 15-year collateral ended the quarter at a spread of 77 basis points over five�year Treasuries (46 basis points tighter). We attribute the modestly better performance of shorter collateral this quarter to a rebound from earlier weakness as 15-year mortgages had widened considerably more than 30-year mortgages earlier in the year (at the end of the third quarter, 15- year mortgages had widened 53 basis points from the start of the year compared to only 24 basis points of widening for 30-year mortgages). Non-agency spreads were flat over the quarter with prime front cashflow tranches ending the quarter at 170 basis points over Treasuries. This was the same level they ended in September, as 10 basis points of spread tightening in December offset similar weakness in October. On an excess return basis for the year, returns on the Bloomberg MBS index were positive (0.68%), recovering from last year’s dramatic underperformance (-2.23%), the second worst year on record behind only 2008.

Paydowns on the Federal Reserve’s mortgage portfolio declined to $14.6 billion in December from $15.1 billion in November. With paydowns well below the $35 billion reinvestment cap, we expect the Fed to continue to allow its MBS holdings to run off its balance sheet. In notable developments, the minutes of the December FOMC meeting contained a discussion of the end of the Fed’s QT program and how to slow the pace of runoff of the Fed’s retained portfolio when “reserve balances are somewhat above the level judged consistent with ample reserves.” In our view, the likely path for the Fed to reduce the pace of balance sheet reduction while moving toward its preferred outcome of an all-Treasury balance sheet, would be to reinvest Treasury maturities and paydowns on its MBS holdings into Treasuries.

After reaching the highest levels seen since the year 2000 in October, mortgage rates slid lower over the remainder of the quarter as interest rates rallied under the assumption that the Fed is in the process of pivoting away from its hiking cycle. The Freddie Mac 30-year mortgage commitment rate fell 93 basis points over the quarter to 6.42%, essentially flat compared to the rate seen a year prior (6.41%). Notably, the drop in rates all happened in November and December as mortgage rates rose over the year to peak at 7.79% in October. While lower mortgage rates are a positive for housing affordability, home buyers still face challenges. Despite the slide in rates, most mortgages still remain outside of the refinancing window and prepayment speeds remain muted. January’s prepayment report showed 30-year Fannie Mae mortgages paying at 4.3 CPR in December, flat to November’s print, while 15-year mortgage prepayments increased 4% to 5.4 CPR in December from 5.2 CPR in November. Bolstered by tight inventory levels, home prices, as measured by the Case-Shiller National Home Price Index, have moved higher for nine straight months. December’s release showed home prices are up 4.8% year-over-year on a national level through October, the largest rate of growth seen during the year, despite mortgage rates peaking that month. Eleven of the 20 metro markets tracked by Case-Shiller showed month-over-month price increases and all but one (Portland) posted positive annual price gains. On the regulatory front, the Federal Housing Finance Agency (FHFA), which regulates Fannie and Freddie, announced increased conforming loan limits in November. The new limit for 2024 will be $766,550, an increase of $40,350 from 2023’s level, which under the FHFA’s methodologies matches the 5.56% increase in home prices between the third quarters of 2022 and 2023. For “high cost” areas (those where 115% of the local median home value exceeds the conforming amount), the limit was increased to $1,149,825 from $1,089,300, which represents 150% of the conforming limit.

Despite the trend lower in mortgage rates, high prices and limited inventory continue to constrain housing sales numbers. December’s report showed November existing home sales at a 3.8 million annualized pace, a 0.8% uptick compared to October’s pace (which came in 4.1% below September) and the first increase in six months. The inventory of unsold homes slid 1.7% to 1.13 million, or the equivalent of 3.5 months’ supply at the current sales pace. Realtors consider anything below five months of supply as indicative of a tight housing market. New home sales also fell over the course of the quarter, capped by an unexpected 12.2% slump in November to a 590,000 annualized pace, a one-year low. Economists had been projecting a 690,000 sales rate. Although more volatile, new home sales are considered a timelier gauge of the market than sales of existing homes (new home sales are calculated when contracts are signed rather than when contracts close which is the case for existing home sales). In line with the lackluster sales figures, home builder sentiment dropped for four months in a row before rebounding slightly in December with the National Association of Home Builders sentiment index coming in at 37. Despite the recent drop in mortgage rates, the NAHB reported that 60% of developers are still extending incentives to potential buyers. In addition, 36% of builders reported cutting prices in December, which matched November’s numbers and reflected the highest percentage share seen in 2023.

The October release of the Fed’s Senior Loan Officer Opinion Survey, reflecting sentiment in the third quarter, showed banks tightened standards for all categories of residential real estate loans other than GSE eligible loans, for which standards were unchanged. Overall, banks reported weaker demand for residential real estate loans. As part of a set of special questions in the survey, banks were asked about their reasons for changing their lending standards over the third quarter. The most frequently cited reasons were a less favorable or more uncertain economic outlook, reduced risk tolerance, a deterioration in the credit quality of loans, concerns about funding costs, a deterioration of customer collateral values, concern about the adverse impact of legislative changes, supervisory actions, or changes in accounting standards, concern about deposit outflows, and a deterioration in or desire to improve liquidity.

Portfolio Actions: Portfolio Actions: Over the course of the fourth quarter, we generally maintained or slightly decreased our RMBS exposure. As in the third quarter, the decrease in exposure was generally the result of the reinvestment of mortgage paydowns into other spread sectors rather than the outright sale of our existing RMBS holdings.

Outlook: Going forward, we expect to maintain or perhaps modestly increase our RMBS allocation across all of our strategies. Any increase would be dependent upon mortgages trading to an attractive OAS threshold relative to other spread products. As in the third quarter, we continued to add opportunistically to our short-tenor non-agency holdings but are avoiding non-Qualified Mortgage (non-QM) tranches in favor of the non-performing / reperforming loan (NPL/RPL) subsector where prepayment speeds are less determinative of overall returns. In addition, we believe the single-family rental (SFR) subsector offers value. In our view, the current affordability challenges facing home buyers and the overall shortage of single-family housing is supportive for that market. However, we remain cognizant of the reduced liquidity of non-agency tranches relative to agency-specified pools.

Performance: Our RMBS positions generally contributed positive excess performance to the portfolios over the quarter after adjusting for their duration and yield curve posture. The one exception was in our five-year strategy where weakness in our non-QM and Prime Jumbo holdings was sufficient to counteract the positive contribution of our agency specified pool positions. The net result was a slight negative performance for the quarter (essentially flat). Our specified pool holdings were mostly positive with notable outperformance in our 1–3-year strategy led by our seasoned 15-year 3.5% coupons. Specified pools were flat in our Cash Plus strategy, which has limited exposure to seasoned 15-year 2.5% coupons. Our CMO holdings were generally positive with the exception of our five-year strategy where they were flat due to weakness in one of our agency “PAC” holdings.

Municipals

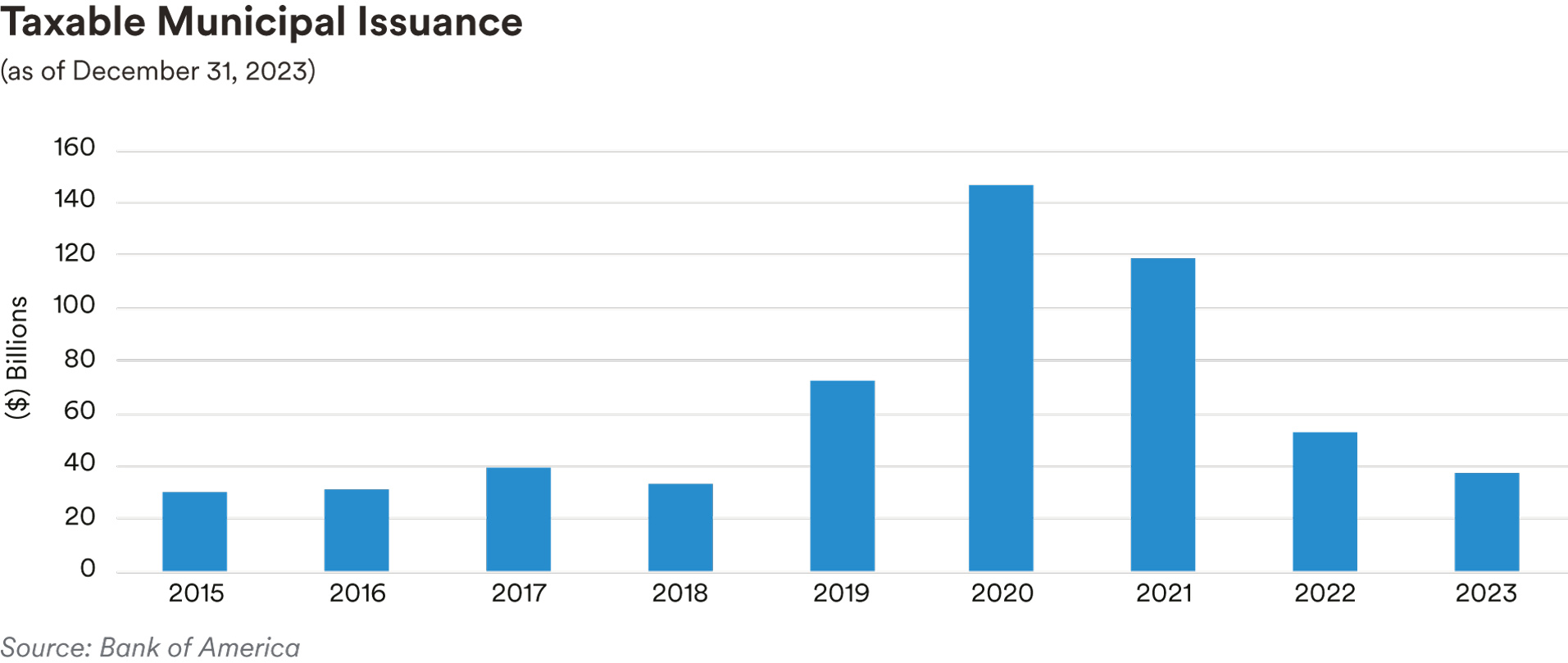

Recap: Total new issue supply was $99 billion in the fourth quarter and as a component of total supply, taxable municipal issuance was $9 billion, 35% higher on a comparative-period basis. While we experienced a slight uptick in taxable supply during the fourth quarter, total 2023 taxable supply was 31% lower than 2022’s issuance. The increase in supply coupled with slightly wider credit spreads in the front part of the municipal market curve resulted in negative excess returns for the sector. For the quarter, the ICE BofA 1-5 Year U.S. Taxable Municipal Securities Index had a total return of 2.99% versus the ICE BofA 1-5 Year U.S. Treasury Index return of 3.10%.

Credit fundamentals, as demonstrated by S&P’s upgrade-to-downgrade ratio of 4.4 to 1 over the first two months of the fourth quarter have continued to be healthy. Notable ratings actions during the quarter included upgrades on several state general obligation issuers by Moody’s, S&P and Fitch. The State of Ohio was upgraded to Aaa from Aa1 by Moody’s and to AAA from AA+ by S&P. Fitch upgrades included the State of Illinois to A- from BBB+ and the State of Pennsylvania to AA from AA-. Bolstered reserves along with able management of dealing with spending pressures and the implementation of necessary budget adjustments were noted as drivers of the upgrades.

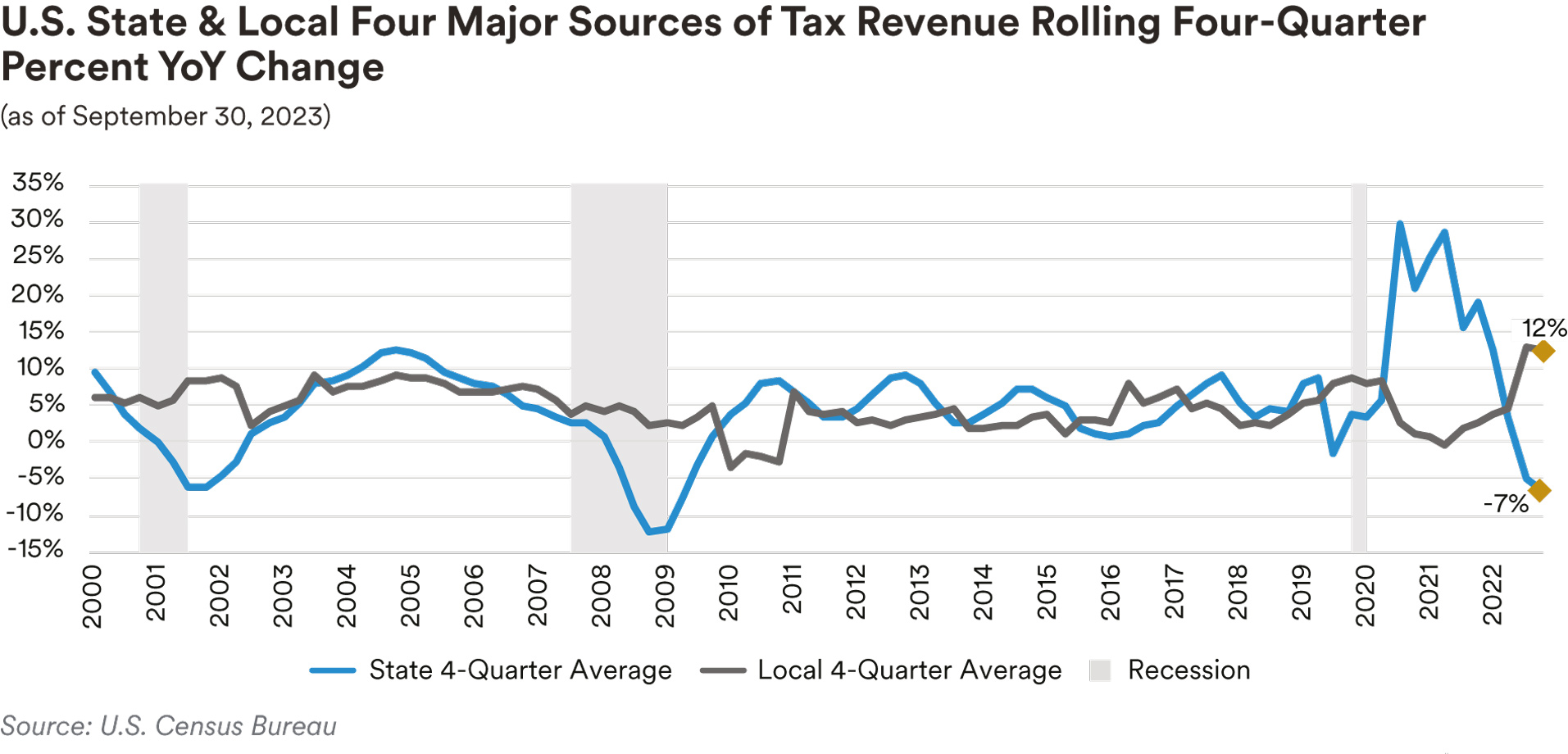

Based on U.S. Census Bureau data collected for state and local tax revenues through September 30, 2023, state receipts continued their negative trajectory while receipts at the local level continued to show growth from the four major tax sources (personal income, corporate income, sales and property taxes). The graph below highlights the decline in revenue receipts at the state level and an increase in revenues at the local level when comparing year-over-year percentage change in revenues from these major sources on a trailing four-quarter average basis.

We continue to monitor pension funding levels that can impact state budgets with lower levels having the potential to stress balance sheets. One indicator we monitor is Milliman’s Public Pension Funding Index, which is comprised of the 100 largest U.S. public pension plans. This index fluctuated with increased market volatility during the first two months of the quarter. The Index decreased to 73.2% at the end of September from 75.3% in August, and then declined further to 71.4% at the end of October, the lowest reported monthly level since October 2022, also 71.4%. The index rebounded in November to an estimated 75.9%. The index remains well below the peak of 85.5% reached at year-end 2021.

We continue to monitor pension funding levels that can impact state budgets with lower levels having the potential to stress balance sheets. One indicator we monitor is Milliman’s Public Pension Funding Index, which is comprised of the 100 largest U.S. public pension plans. This index fluctuated with increased market volatility during the first two months of the quarter. The Index decreased to 73.2% at the end of September from 75.3% in August, and then declined further to 71.4% at the end of October, the lowest reported monthly level since October 2022, also 71.4%. The index rebounded in November to an estimated 75.9%. The index remains well below the peak of 85.5% reached at year-end 2021.

Portfolio Actions: Our allocation to taxable municipals decreased in our shortest duration strategies and exposure levels remained constant in our other strategies over the fourth quarter. On the new issue front, we added credits in the local government and transportation sectors. We were also active in the secondary market, adding to high-quality issuers in the airport, essential service, highway, and state obligation sectors. In addition, we added exposure to a short-tenor healthcare issuer.

Outlook: While municipal credit fundamentals have recently proven their resiliency with issuer balance sheets and reserves healthy overall, we feel we may have reached a peak in municipal credit conditions. Tax collection data for the second quarter of 2023, as reported by the Urban Institute, shows total state tax revenues declining 15.7% in real terms on a year-over-year basis. Should we enter into a period of an economic slowdown, revenue streams from personal income and sales taxes would continue to trend lower, further pressuring issuer revenues, particularly on the state level. Partially mitigating these concerns is conservative budgeting practices. The National Association of State Budget Officers expects spending growth to decelerate in fiscal 2024 following two years of double-digit increases. An estimated increase of 6.5% is expected compared to preliminary actual levels for fiscal 2023, following a growth rate of 11.8% in fiscal 2022 and 16% in fiscal 2021. Further mitigating these concerns are historic reserve levels and the strength of state balance sheets. In revenue bonds, one sector that has been facing ongoing pressure is healthcare. Inflation and labor shortages have pressured hospital systems as increased labor and supply costs have resulted in declining operating margins within the sector. However, we have experienced a rebound in margins with a few factors contributing to this recovery. First, the usage and pricing of contract nurses has declined significantly as healthcare systems have ramped up their direct hiring of nurses helped by offering better wages and greater flexibility in working arrangements. Secondly, volumes of health services have increased markedly as people have resumed using health services at a more normal or pre-pandemic rate and, in some cases, have caught up on health care that had been postponed during the COVID-19 pandemic. Thirdly, healthcare systems have gotten serious about cost containment with many systems undertaking staff reductions of around 2% of headcount, concentrated in non-patient-facing roles, to get cost structures back in line with revenue potential. With that said, average margins are still 150-200 bps below pre-pandemic levels and it will likely take another 1-2 years of expense leverage before margins recover back to pre-pandemic levels. We have selectively added to our exposure in this sector favoring hospital systems that have been open to evaluating their operations and have taken the necessary cost cutting measures and are reducing the use of contract labor with an emphasis on improving operating margins.

We remain defensively biased and selective in evaluating purchases for our strategies, with a focus on issuers that demonstrate strong credit fundamentals. While we remain constructive on overall credit fundamentals in the municipal space, we are cognizant of the potential for pressure on budgets with changes in the macroeconomic landscape and focus on issuers with operating and financial flexibility, along with demonstrated management ability and willingness to make necessary budget decisions/adjustments. In an investment environment characterized by macro market volatility and economic uncertainty, we view an allocation to the municipal sector as a defensive alternative to other spread sectors and plan to add to the sector as opportunities arise.

Performance: Our taxable municipal holdings generated mixed performance across our strategies in the fourth quarter. On an excess return basis, some of our better performing sectors included Local Tax-backed issues and Not-for-Profit. Holdings in the transportation sectors were mixed but positive in aggregate while select holdings in the Essential Service and State Obligations areas generated negative excess returns.

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors. This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets. In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address 1 Angel Lane, 8th Floor, London, EC4R 3AB, United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102-0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) under the registration entry Director General of the Kanto Local Finance Bureau (FIBO) No. 2414, a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

MIMEL: For investors in the EEA, this document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.

1 As of December 31, 2023, subsidiaries of MetLife, Inc. that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors include Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), MIM I LLC, MetLife Investment Management Europe Limited, Affirmative Investment Management Partners Limited and Raven Capital Management LLC L0224038016[exp0824][Global]