At the beginning of 2026, we were anticipating a year when market leadership would pivot back to the U.S., given that global growth drivers remained narrowly focused on AI and largely U.S.-based. Taiwan and Korea supply much of the chips that drive AI, and several mega-caps from these two countries have almost single-handedly pulled emerging markets into the winners’ circle. Despite intervening events that could have threatened to derail AI’s secular take-off (most notably tariffs and the war in Iran), other developments have only strengthened it. And headlines notwithstanding, the U.S. has extended its lead in the AI-driven productivity race by demonstrating a sustainable monetization model.

Beyond AI, the U.S. also witnessed a much greater-than-expected broadening in first-quarter earnings. Private-sector, supply-oriented investment is beginning to replace government-led support for demand, which had been the driver for most of the post-COVID period (remember the CARES Acts 1 and 2, the Infrastructure Act, the CHIPS Act and the Inflation Reduction Act). The CARES Acts, among other priorities, provided substantial funding for state-level healthcare and educational efforts, which for years skewed employment higher in these areas. That funding is now expiring.

We see the early stages of an investment boom focused on something new, with a long development runway ahead—not late-cycle excess, with investment activity focused on adding to existing capacities. Many comparisons are made between AI’s ascendance and the internet. If this were the 1990s, think 1996, when a massive multi-year investment cycle fueling internet commercialization and the telecommunications infrastructure had begun to accelerate in earnest (and wasn’t yet overdone). When the comparison is funding sources, we see the period ahead as more analogous to the build-out of the railroads: highly capital-intensive, new and definitively game-changing, and funded by debt issuance. The internet was funded by equity issuance. AI increasingly will be funded by U.S. investment grade (IG) debt issuance. Where the issuance swells, real rates and spreads will push higher over time. We favor fixed income outside of areas where issuance keeps swelling.

These dynamics contribute to a constructive multi-asset view. Today’s global growth engine is narrow, led by AI, with a long runway ahead. It’s unlikely to be a smooth ride. Even with solid and improving fundamentals, crowded positioning among retail investors and trend followers could amplify volatility, while geopolitical shifts continue to rewrite yesterday’s rules of the road. The global economy is just beginning to shake off inflation waves created by two disruptive supply shocks that appear to be cresting—tariffs and energy prices. Meanwhile, the upfront capital-intensity of the AI build-out has produced a third inflationary wave that is newer and that will be with us for some time. Unlike the earlier waves tied to tariffs and energy, this demand-driven impulse comes from the AI build-out itself, raising producer prices before AI-driven productivity gains can begin to ease services inflation. Central banks are going back to the basics: influencing the short end of yield curves to implement monetary policy, while allowing supply and demand to determine the longer end of sovereign curves, with supply from AI issuance and fiscal dominance both powerful drivers of rising real rates.

These new dynamics follow decades of underinvestment by the West, as capital intensity was outsourced to China following its entrance into the World Trade Organization (WTO) 25 years ago. AI’s capital intensity is being funded on top of fiscal deficits that pushed higher after COVID in nations like Europe and Japan, which are just now beginning to wrestle with the need for higher defense spending in an increasingly might-makes-right world.

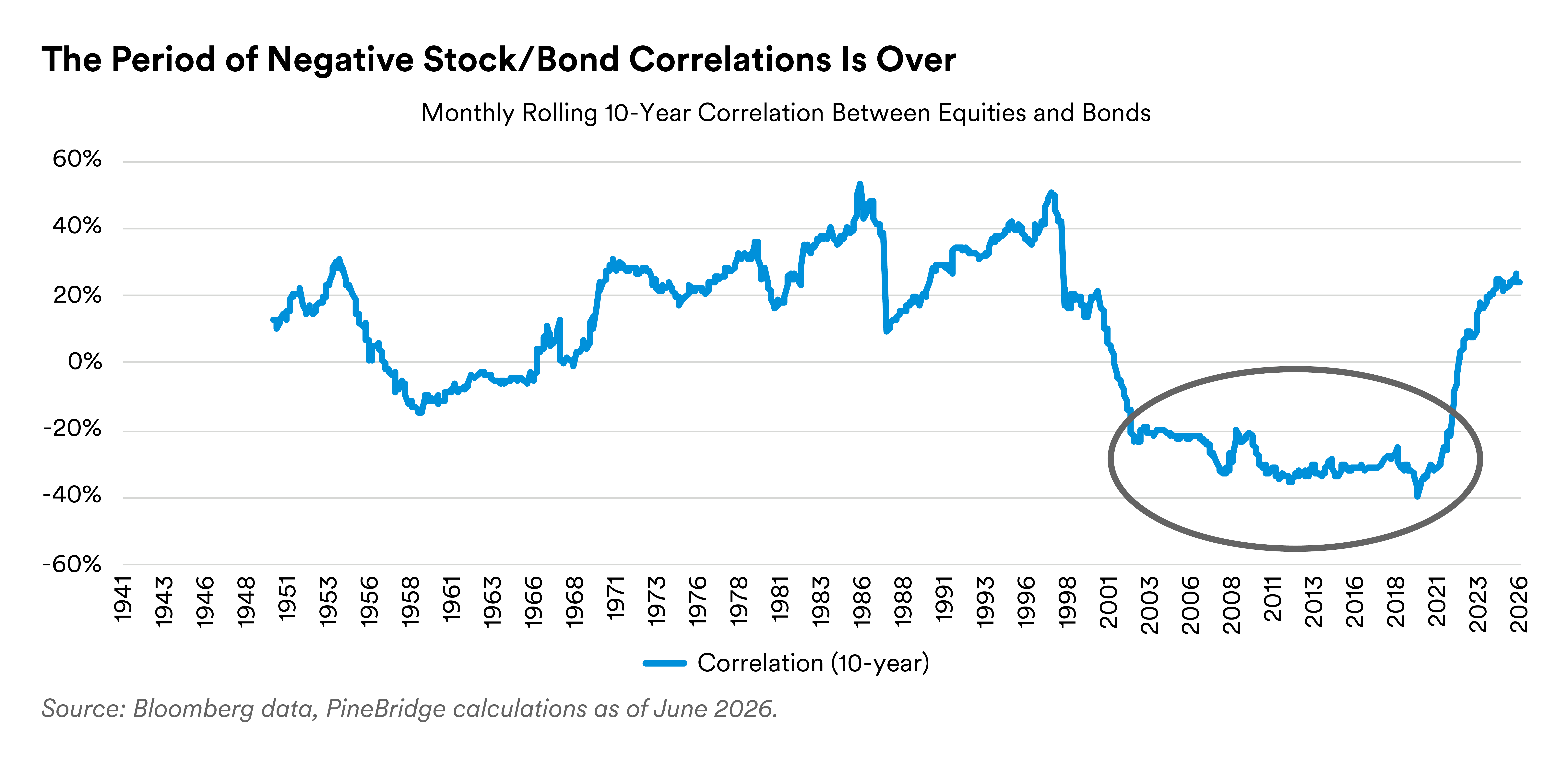

Meanwhile, traditional stock-bond diversification looks much less effective than it was from 2001 through 2021 (see chart below). The negative correlation between stock and bond returns has now turned mildly positive, which has been the historical norm outside of the peculiar 20-year period highlighted below.

Notably, the secular nature of today’s investment-led economy argues for staying invested in growth assets, particularly equities, while the investment boom’s upward tug on real interest rates is a drag on fixed income returns, which calls for “diversifying your diversifiers” through selective use of commodities, risk premia and cash-plus-alpha strategies. In recent years, gold was also on that list for us. However, higher real rates are gold’s enemy, and the new Federal Reserve Chair, Kevin Warsh, also isn’t a friend of gold, with his inclination to shrink the balance sheet gradually over time (dampening currency debasement fears that drive gold) and then to ensure that crisis-oriented policies like forward guidance and QE are used only in crises.

The most important shift since year-end is that AI has moved from a period of rising capital intensity with mere promises of return on investment to showing tangible signs of monetization and contribution to profits — at least for hyperscalers that can justify these investments with payback through their cloud services, which benefit from AI usage. In 2025, markets were right to question U.S. exceptionalism, simply because investors were witnessing the largest tech companies moving from asset-light to asset-heavy business models as they committed vast capital to data centers, compute and infrastructure before monetization models had proven themselves. What was clear was that return on assets (ROA) and return on invested capital (ROIC) were declining for these index behemoths, as were these mega-caps’ price/earnings ratios, which placed a meaningful drag on U.S. large-cap indexes. Of course, tariffs and other uncertainties also played a role.

That was 2025. Early in 2026, Anthropic demonstrated practical yet powerful AI applications in the form of agentics — which could prove to be AI’s killer app — as well as the Claude Workbench. Enterprise is sold on the benefits, with a race to the future driving token usage and the revenue implications becoming harder to dismiss. Year-over-year earnings estimates of the providers that had been decelerating throughout 2025 inflected sharply higher in the first quarter of 2026. The point is no longer that AI is exciting; it is that users are finding applications valuable enough to pay for. “Freemium” packages driven primarily by the number of users are giving way to usage-based pricing (in addition to user counts), with enterprise companies starting to see bills that reflect actual consumption. While this might foreshadow a short-term pause in adoption as enterprises reevaluate the costs, we expect returns to prove highly compelling overall, and that adoption and revenue acceleration will follow. It’s useful to remember the early experience of cable and internet providers. Once users were hooked on these first-of-their-kind services, providers spent the next decade learning how to monetize their newfound market power — through direct price increases for cable companies and advertising for internet providers. Then came bundling into new products and markets.

In 2026, the U.S. also appears to be widening its lead over China. One year after the launch of DeepSeek, fears that China could rapidly overtake the U.S. in large language models have not materialized. While open-source models may scale quickly, giveaway models do not generate the revenue needed to monetize and justify investments in data centers, power and the broader AI ecosystem. Currently, only ByteDance has announced that it will enter this race, and its announced investment, along with the central government’s, is tiny relative to competition coming out of the U.S. While that could still change, the gap meanwhile is rapidly widening in the U.S.’s favor.

First-quarter earnings reinforced our views. Expectations called for deceleration among the largest technology companies, with slow acceleration elsewhere. Instead, large tech companies delivered the strongest upside surprises, while most other sectors also beat expectations.

Energy also meaningfully outperformed, but that reflected the cresting U.S.-Iran conflict rather than a new secular earnings breakout. While the improvement within technology centered on the hyperscalers, the broadening beyond tech and energy suggests that profitability is strengthening long before the productivity payoff from AI has even begun. This transpired even though the economy was not particularly strong in the first quarter. U.S. profits still step-functioned higher, suggesting a faster productivity trajectory even before the benefits of AI kick in. Over the past 20 years, public equities have become much more aggressive in how they run their income statements, narrowing the gap with private equity in this regard — yet the public firms are applying this sharper mindset to higher-quality franchises.

Inflation remains central to our outlook. We make a distinction between persistent inflation and temporary supply shocks. The stock market has been willing to nervously look past what it views as temporary supply shock-induced inflation. Tariffs did lift select goods prices, yet this year-over-year inflation impulse is visibly fading with the “anniversary-ing” of tariffs. Energy is similar. The recent escalation in the Gulf raised legitimate medium-term concerns about oil, but the global system proved much more flexible than most expected. China ended its reserve build-up in recent months, as well as aggressively switching from oil to coal and accelerating their shift toward renewables. China’s efforts also drove home the message that it was no longer willing to stand by Iran as the war threatened to disrupt the global economy — including China’s exports, which are crucial to China at a time when the nation is grappling with a stagnant domestic economy. Higher U.S. hydrocarbon exports and alternative supply routes also played meaningful secondary roles in preventing oil prices from bending parabolically higher. Oil hovering below $80, while not benign, is still nowhere near the recession-inducing or globally destabilizing prior predictions of $150-plus oil by the end of May.

A more critical judgment call will be the inflationary impact of AI. While most acknowledge that AI productivity benefits, when they arrive, will support medium-term disinflation, the build-out is turning out to be quite inflationary upfront. AI is driving booming demand for everything related to building data centers. These demand-driven inflationary forces are going full-tilt, yet will continue to inflate producer prices for many years to come, with some degree of pass-through to consumer prices — the Fed’s primary focus. For instance, Apple has prepared markets for higher iPhone pricing, given the pronounced spike in memory costs as one result of the AI build-out. When use cases pan out, AI should begin disinflating services — the largest slice of the U.S. economy and of consumer inflation indexes. Our view is that at some point in 2027, perhaps early on, this productivity-driven supply will begin to overtake the upfront demand pressures from AI’s build-out. This judgment comes from listening to companies discuss their use cases and the timing of such benefits.

The challenge will be bridging this period between AI’s upfront costs and the subsequent productivity payoff. Stocks are more likely to look past this timing issue than rates and FX. That poses a challenge for Kevin Warsh. The new Fed chair may need to hike rates once or twice this year to back up his call for price stability, before cutting rates two or three times next year if AI’s net disinflationary impulse fails to show up in time. Meanwhile, Warsh appears to be slow-walking rate hikes by erecting five task forces to study a complete revamp of the Federal Reserve. Yet all told, two of three main inflationary impulses (tariffs and the Iran conflict) are now fading, whereas several months ago, all three (including the AI build-out) were still pushing up prices.

Given time, AI appears poised to create powerful results for individual business models and the economy alike. Such supply-driven expansion may sidestep the classic acceleration in demand-driven inflation that tends to accompany faster growth. The upside case is not just that AI boosts technology stocks; it is that its productivity benefits can spread to a broader swath of users, thereby raising the economy’s speed limit. Of course, there will be winners and losers within and across industries and countries, as is the case with every technological breakthrough. Yet the net effect, more often than not, is a positive one.

We remain constructive on equities. U.S. equities lagged in 2025 as investors questioned AI CapEx, and sentiment toward rising asset intensity led to declining P/E’s for many of the biggest weights in the S&P 500. In 2026, that pressure is reversing amid growing evidence that capital spending is translating into rising usage, revenue and earnings, along with upward-inflecting ROIC. Capital is also being aimed at bottlenecks, such as semiconductor supply chains, although the masters in Taiwan and Korea are remaining highly disciplined, and China’s chips are being absorbed domestically. The U.S. AI build-out has tugged along a handful of mega-caps in Taiwan and Korea that have soared to such heights that three stocks alone have essentially lifted the emerging equity index.

We have also become increasingly interested in alternative energy, which continues to benefit from climate urgency and now, from AI’s insatiable demand for electricity. Growing concerns about sourcing too much energy from the now structurally unreliable Strait of Hormuz adds to this momentum.

Broader first-quarter earnings strength also suggests that the profit cycle is widening, with or without an accelerating economy, thus reducing reliance (though slowly) on a narrow group of mega-cap companies and supporting a more durable equity advance. The shift from fiscal support to private investment as the driver of the economy also matters: Pandemic demand props have flatlined and are running out of funding. Powerful post-COVID fiscal support for education and healthcare led these categories to dominate job formation for years, but those allocations are now approaching their tenure and funding limits. If and when private investment and productivity take over, which today’s resilience suggests is beginning to happen, equity markets will likely become emboldened by this more sustainable growth model.

In the near term, we expect periodic pauses in AI adoption as companies manage the related costs, and investors reassess how quickly the productivity gains will arrive. Consumption-based AI bills could slow usage temporarily as the move away from “freemium” usage exposes unexpected enterprise bills. But token costs are poised to fall significantly as new chip generations arrive. Dramatic improvements are already visible, supporting broadening adoption of AI well beyond big enterprise-leading firms. We believe investors should stay focused on the medium-term direction: Like the railroads of an earlier era, AI investment is now moving from a speculative build-out phase toward measurable and broadening economic contributions. Bubbles may eventually form, but today’s valuations do not yet suggest excess: Price-to-earnings ratios are barely keeping up with growth, and the best-positioned hyperscalers still trade at only modest premiums to market averages despite years of growth runway ahead. So any bubbles are likely a long way off.

Fixed income requires a different lens than it has in the last several decades. Years of outsourcing capital intensity to China after it entered the World Trade Organization (WTO), deleveraging following the financial crisis and extreme monetary policies in the form of QE and (very) forward guidance kept real rates suppressed. In what we call the “Stall Speed” nature of the dozen years following the financial crisis, a growth relapse would have been a boon to high-quality bonds and a bust to growth assets like equities. Therefore, the correlation between Treasuries and equities became persistently and meaningfully negative.

Against that backdrop, high-quality bonds became super-diversifiers for equities — a regime that was historically unusual, and one we now refer to as the “old abnormal.” Today’s economy is miles away from the Stall Speed era that gave bonds these diversification superpowers, a period defined by loose physical capacity, output gaps and very easy money. Now the environment is shifting toward a firmer physical world complemented by a firm and firming monetary backdrop. This means the negative stock-bond correlation is no longer warranted and, not surprisingly, no longer exists. The GDP growth mix ahead is also far more capital-intensive, and real interest rates have risen in tandem. Investment-led booms are better for growth assets than for safety assets like high-quality bonds, which finance much of the boom but often suffer at the end of these periods, despite backing the strongest firms of the era.

While short-term rates have risen mainly on higher interim inflation expectations, beyond three years, the increase has been driven by higher real rates. Issuance in the longer end is rising far faster than the supply of savings tied up for the long term. Rates are the equilibrator. Central banks have limited influence over the long end when they stick to managing overnight rates, which is the direction we expect the Fed under Chair Warsh and central banks more broadly to revert to. A typical post-crisis-inspired question today is “What level of rates will break the stock market?” Fortunately, the rise in longer-term yields is signaling robust and resilient growth ahead, pulled forward not only by AI but also a by a convergence of new technologies. This means real rate-driven rises in long rates are not necessarily a bearish signal — especially if AI’s ROIC turns out to be well above the cost of debt financing.

Today’s higher real rates also reflect renewed demand for capital in the West after decades of underinvestment following China’s entrance into the WTO. While AI is central to this shift, behind AI lies a parallel need for energy infrastructure, water infrastructure and eventually more ambitious physical infrastructure. National security issues are also being prioritized within private business to secure the nation’s supply chains, sometimes at the request of governments. This investment boom could run for years and will need financing in quantities that stretch the imagination — most of which will be supplied by IG debt issued in the U.S.

Tight spreads often collide with peak economic conditions and the increasingly lax underwriting that comes with extended cycles. While we’ve seen such pockets in this cycle as well, they cropped up in well-flagged private equity software buyouts, where private-market leverage could run far higher than in bank-driven financings. But within the capital markets, which largely exclude most small businesses and the lower end of the K-shaped consumer, today’s tight spreads are not necessarily broadly fragile. The investment-led nature of the cycle ahead provides a layer of growth that otherwise would not have existed, supporting many old-economy credits that stand to benefit from second-order effects of the AI build-out. The existential nature of today’s investment boom (where many firms believe they must use AI to create advantages or that others will) creates a resilient floor under the economy’s growth profile, providing some much needed stability to many credits.

While a more traditional late-cycle playbook would call for moving up in quality ahead of a cyclical downturn and related spread widening, we do not view a recession as likely in the next few years, given the extra layer of resilience from this existentially driven investment-led economy. Thus, spreads should stay “narrow for longer,” with limits to how narrow they can go, yet without such limits on how high-growth assets like equities can climb. Against this backdrop, high yield spreads, while narrow for the asset class, still provide carry above inflation, with duration often much shorter than for the longer-dated U.S. IG paper where issuance is likely to concentrate. We prefer selective credit that can deliver yields exceeding inflation, including parts of high yield and the belly of the curve, while recognizing that further spread compression has limited room to run. We continue to like Asian high yield (ex-China property), which remains weighed down by the broader fallout from China’s property downturn. Select LatAm sovereign credits also look attractive: Several countries are pursuing more market-friendly reforms, offer high real interest rates and stand to benefit economically from a metals bottleneck tied to the AI build-out.

IG is where we expect the mass issuance to keep surprising to the upside, while emerging market credits have not seen the fiscal deterioration so evident in most developed economies. We expect that to continue.

While bonds are still important for preserving capital and purchasing power, their role as a super-diversifier is less obvious than before. As the economy moves toward a potentially hotter regime, investors need to think about diversifying their diversifiers. This argues for a broader toolkit.

Commodity carry and other forms of risk premia can provide diversifying exposures, as can real assets. Cash-plus-alpha strategies benefit when cash yields are above inflation, and the world morphs toward bigger winners and bigger losers, creating better breadth and the potential for more and more effective long/short pairs.

Real estate also deserves attention. Prior productivity-led growth spurts were associated with great wealth creation that favored pockets of real assets.

We remain pro-risk, but not pro-complacency. We favor equities over fixed income, with a bias toward equities with a productivity angle, as either a provider or beneficiary. In credit, we lean more toward high yield than IG, given tight spreads, several years of stronger profits with low recession risk and a bias toward avoiding areas where issuance are likely to set records.

The AI build-out is likely still in early days, with productivity gains only beginning to surface, suggesting a large earnings payday ahead. This supports staying invested, leaning toward growth assets, while using a broader set of diversifiers to navigate a less predictable macro and geopolitical risk regime.

Our midyear message is one of constructive realism. Inflation is not fully resolved, although two-out-of-three primary drivers (tariffs and the Iran conflict) are now heading in a more constructive direction. Real rates are likely to stay high and may slowly trend higher, but unlike the past 20 years, they at least offer fair value — even if they are not yet rich. The AI cycle will not move in a straight line, but evidence points to a stronger private-sector-led investment cycle that could extend the expansion well beyond what fiscal thrusts can deliver, as many governments — particularly in developed markets this time — are hitting their limits at the same time. For multi-asset portfolios, these dynamics argue for a continued leaning toward growth assets, with a selective stance on credit and a more demanding approach to diversification.

Disclosure

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors.

MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world. The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risk, including possible loss of principal; no guarantee is made that investments will be profitable. This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. Views may be based on third-party data that has not been independently verified. MIM does not approve of or endorse any republication of this material. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

In the U.S: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK. © 2025 MetLife Services and Solutions, LLC.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also subdelegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees’ pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.