“There was a strong bifurcation in performance between property types, and that’s something that never happened during prior downturns,” says Will Pattison, head of real estate research and strategy at MetLife Investment Management. Rapid e-commerce growth drove increased demand for warehouses, while offices, malls and retail spaces saw a precipitous drop in demand.

That’s created changed investing patterns. In the past, real estate investors might focus on several property types. “Many institutional investors today are only targeting one or two property types, and that’s a fairly significant difference from how capital markets worked before the pandemic,” Pattison says.

Hedge against inflation

Inflation has been top of mind for many investors, and that could be beneficial for real estate. Commercial real estate has historically shown resilience during inflationary periods. MIM believes with inflation currently at a 40-year high of 8.5%1, real estate is in an usually attractive position, which MIM expects will draw more inflows into the sector.

“Insurance companies usually focus on fixed income investments, but I think you’ll see more of the insurance companies investing in direct real estate through acquisitions and development. More capital could come into the sector from the insurance side because of the recently lowered capital charges,” Merck says. Insurance regulators recently lowered the amount of capital that insurers are required to hold for real estate investments. The change effectively increases the pool of capital that insurance companies can invest into the sector.

A focus on apartments and warehouses

One of the best potential inflation hedges in real estate is apartments. Apartments typically have short-term leases, which can be ideal during inflationary times because owners can better adjust to the short-term impact of inflation by resetting the lease. MIM estimates that apartment rents will increase an average of 3.2% a year through the current decade. Migration out of certain metropolitan areas—such as from New York to Florida—accelerated during the pandemic and will likely impact supply and demand and housing prices in various markets.

MIM Feels another sector to watch is warehouses, which are benefiting from significant e-commerce growth. “I don’t think the market fully understands that online order delivery speeds have been at least as important as the total number of goods being purchased online,” Pattison says.

A few years ago, order fulfillment might take seven days. Today, it’s closer to one or two days—or even a few hours in some markets. That faster fulfillment means e-commerce companies can no longer rely on a handful of supersized regional warehouses. Instead, there’s a need for smaller warehouses located in all major cities. These infill warehouses, or last-mile delivery centers, range from 50,000 to 200,000 square feet, compared to regional or super regional warehouses that are often a million square feet.

“People want a little bit more space. They don’t want to share space or use hoteling to reserve a desk. I think COVID helped solidify that,” Merck says.

Longer term, Merck doesn’t see a significant impact from the growing acceptance of hybrid work. MIM estimates that 9% of the traditional office using employment sectors will become fully remote, up from about 5% before the pandemic. But lessening demand for office space could be partially offset by a slowdown in new office construction. As a result, office leases today in most markets are being signed at pre-pandemic prices. While companies with offices in markets such as New York or San Francisco, which rely heavily on public transit, are more likely to downsize in the near term, MIM believes the impact will be temporary. Not only that, but some of the markets seeing the worst short-term impact may also see the strongest demand over the next decade.

Another real estate sector that saw many vacancies in the last two years was retail, which struggled even before the pandemic due to e-commerce growth and overbuilding. The pandemic accelerated the closing of retail centers that likely would have closed anyway. Of course, not all properties are the same. Merck says there’s been a flight to quality, with higher-end malls with strong sales per square foot bouncing back. “We’re starting to see that play out in a positive way,” Merck says.

In any time of crisis, new opportunities appear. “Real estate has made a really good comeback, both in 2021 and especially this year,” Merck says. The last two years were tumultuous for some parts of real estate, but buoyed by high inflation and rising consumer demand, we believe overall the sector’s outlook is bright.

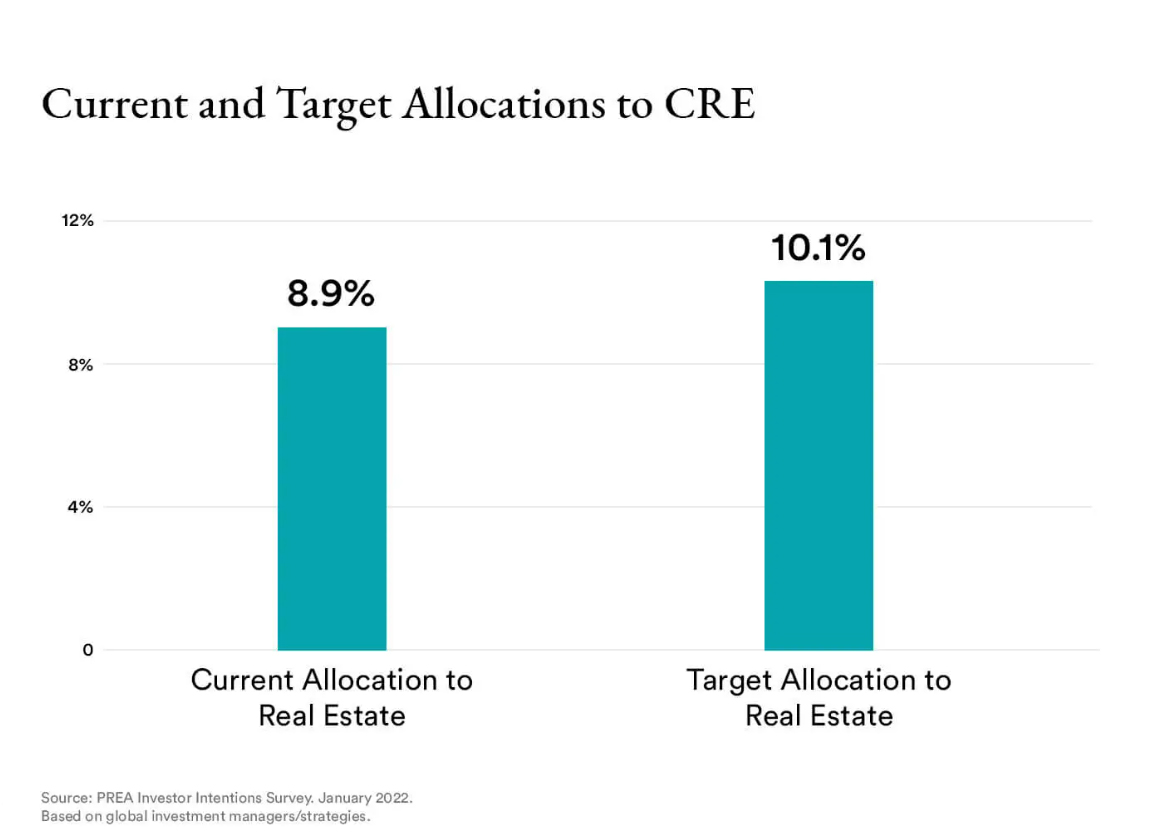

More Capital Expected High inflation and low interest rates are pushing insurance companies and other investors to direct capital into commercial real estate.

Endnotes:

1 U.S. Bureau of Labor Statistics, May 2022

Disclaimer:

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

This document has been prepared by MetLife Investment Management (“MIM”) solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets.

In the U.S. this document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address Level 34 One Canada Square London E14 5AA United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK and EEA who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as implemented in the relevant EEA jurisdiction, and the retained EU law version of the same in the UK.

MIMEL: For investors in the EEA, this document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Asset Management Corp. (Japan) (“MAM”), 1-3 Kioicho, Chiyoda-ku, Tokyo 102-0094, Tokyo Garden Terrace KioiCho Kioi Tower 25F, a registered Financial Instruments Business Operator (“FIBO”) under the registration entry Director General of the Kanto Local Finance Bureau (FIBO) No. 2414.

For Investors in Hong Kong: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”).

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

1 MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors, including: Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Asset Management Corp. (Japan), and MIM I LLC and MetLife Investment Management Europe Limited.