We expect that growth will be modestly positive throughout 2026. The wealthier strata of consumers continue to spend, supported by the strong market valuations and stability in the labor markets.

Specific areas of business expenditure have resumed following tariff-induced bouts of uncertainty, as have those portions of business expenditures relating to the boom in AI adoption and its supporting infrastructure.

Concerns about tariff policy appear to have peaked earlier in the year across substantial parts of the market and the economy.

Our primary economic concern for 2026 is the labor market. Businesses appear to be weathering the policy uncertainty and tariff-induced cost increases by cutting costs and delaying investment without resorting to wholesale layoffs. This is a good thing, but new labor market entrants are not being fully absorbed, and we expect that to continue into the new year. We expect firms to remain cautious about hiring throughout 2026 even as they restart major investment projects. Younger workers and those with fewer in-demand skills are likely to find it difficult to secure jobs even as the unemployment rate remains low by historical standards.

We place a 30% probability of recession on the U.S. economy in 2026, with risks primarily emanating from renewed concerns about tariff policy, the relatively narrow base of economic strength, and the potential for substantive market corrections.

We expect the Federal Open Market Committee (FOMC) to cut rates again before year-end 2025 and to continue to cut next year. Despite inflation still being above its 2% target (for nearly five years now) and heading in the wrong direction, there appears to be rising concern among FOMC members around

Higher U.S. tariffs and slower global trade growth are expected to continue to weigh on Europe’s economic prospects in 2026. While trade agreements were reached on baseline U.S. tariff levels of 15% for the EU and 10% for the U.K., confidence that these deals will stick is tenuous and the negative impact on Europe’s exporters will continue to play out next year. Nevertheless, partly based on an assumption that the peak level of trade uncertainty is behind us, we forecast a moderate pick up in the pace of euro area growth to 1.3% in 2026 from around 1% this year, and for growth in the U.K. to remain steady at around 1.3%.

Private consumption should be supported by a robust euro area labor market, positive real wage growth, and looser monetary settings. The European Central Bank looks to be near or at the end of its easing cycle. However, the lagged impact of its having already halved its deposit rate since mid-2024 (to 2%) should help support the growth outlook. Fiscal policy is set to be moderately looser at the euro area level as Germany’s government begins to ramp up spending on infrastructure and defense.

In the U.K., meanwhile, we anticipate more weakening of the labor market along with a slowing of real wage growth and easing of inflationary pressure after its late-2025, policy-driven rebound. The Bank of England has reduced its bank rate by 125bps since July 2024 to 4% and we expect it to continue its cautious rate cutting cycle into H1 2026 (to a terminal bank rate of 3.25%).

In China, we expect GDP growth to remain generally subdued at around 4.5% in 2026. Headwinds would be drags from softer external demand via U.S. tariffs and the ongoing anti-involution campaign against excess competition and capacity, which would crimp production, investment, and employment. The property sector will also likely remain challenged. We expect continued policy support to serve as a partial offset, with fiscal policy taking the lead to encourage consumption and investment as well as addressing local government debt risks.

On the inflation front, measures to promote consumption and address excess capacity, as well as base effects from 2025, should lift the GDP deflator out of negative territory by the middle of next year, while CPI should average around 1%.

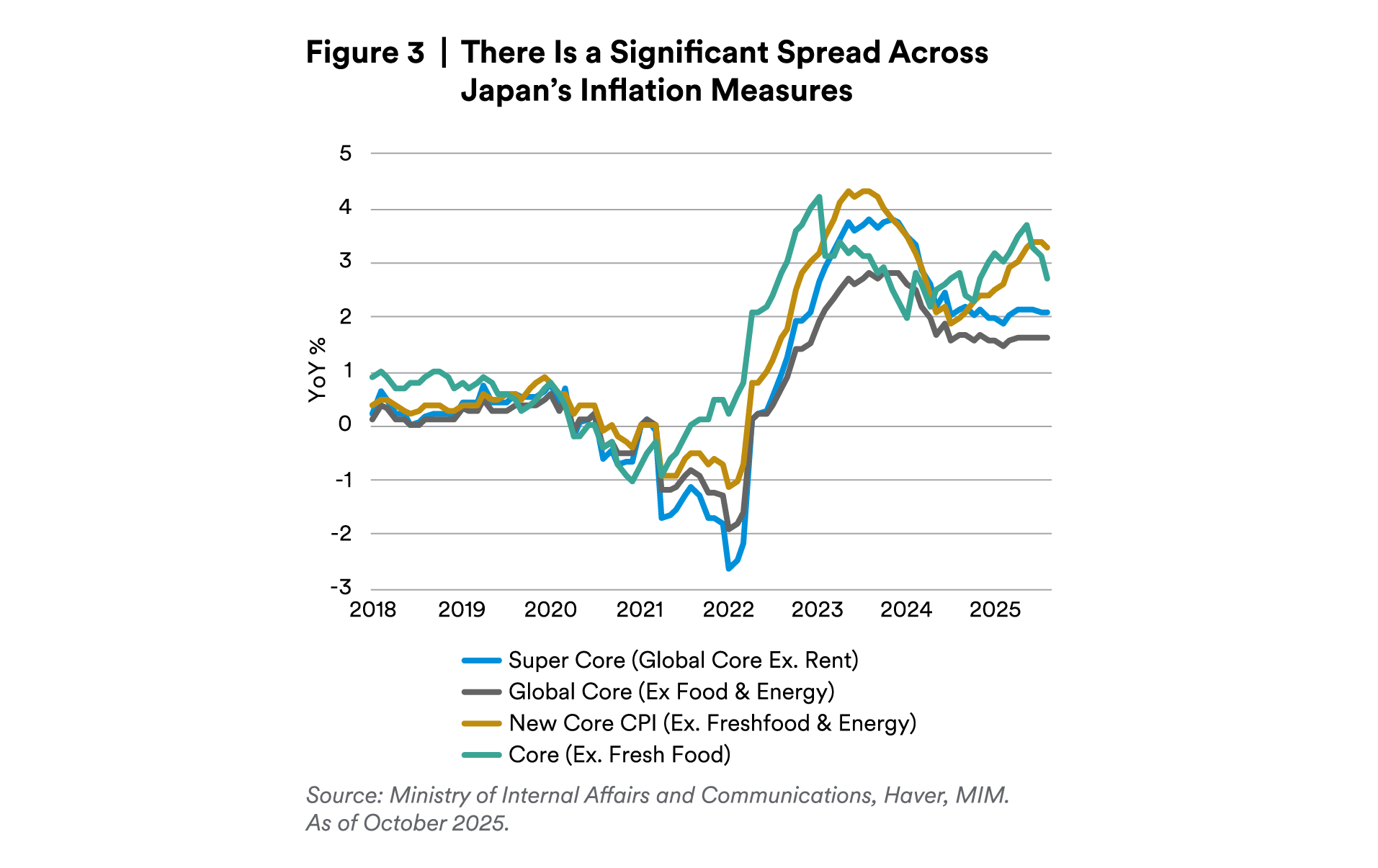

In Japan, we expect the economy to grow by about 1% in 2026, roughly in line with this year and remaining above potential. We expect domestic demand to drive growth. With inflation slowing, real wage growth should gain momentum, supporting household consumption. Capital expenditures are likely to remain supported by structural demand for AI and digitization.

Whereas our baseline for 2025 has been for the Bank of Japan (BoJ) to remain on hold, we believe it will more actively consider hiking the policy rate in 2026 if it gains more comfort around global growth and domestic “underlying inflation”, which has been more subdued than core CPI readings to date. Core CPI readings remain above 2%; however, Global Core CPI (best approximating the BoJ’s “underlying inflation” assessment) has hovered around 1.5%.

Another key driver of monetary policy will be fiscal policy from the next government. For that, we need to wait for the political dust to settle.

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors.

This analysis is not intended for distribution with Retail Investors. This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets.

In the U.S.: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK. © 2025 MetLife Services and Solutions, LLC.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also subdelegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees’ pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being issued by MetLife Investments Asia Limited (“MIAL”), a part of MIM, and it has not been reviewed by the Securities and Futures Commission of Hong Kong (“SFC”). MIAL is licensed by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.

1 As of March 31, 2025, subsidiaries of MetLife, Inc. that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors include Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Investment Management Japan, Ltd., MIM I LLC and MetLife Investment Management Europe Limited.