During the past several weeks, the leveraged credit markets have arrived at a highly complex macroeconomic crossroads. Sticky inflation data — underscored by a hot, year-over-year consumer price index (CPI) print — collided with volatile geopolitical headlines that briefly pushed crude oil prices near multi-year highs. This hardening macro backdrop completely upended the rates backdrop. Treasury investors switched from anticipating near-term Federal Reserve (Fed) policy cuts to pricing in explicit interest-rate hike risks, with forward markets placing an overwhelmingly high probability on a final interest-rate increase by the winter voting session. This sudden upward trend in Treasury rates brought back a tactical bid for floating-rate asset classes. Leveraged loans briefly overtook high yield bonds in total return performance, year to date, supported by the carry component, given the healthy yield premium over fixed-rate corporate debt. Concurrently, strong demand allowed issuers to run a massive refinancing wave, expanding the repriceable share of the institutional loan index to its highest level of the year.

However, we view this floating-rate outperformance as a near-term phenomenon. A rising percentage of lower-quality loan issuers face a maturity wall over the next two years. With policy rates staying higher for longer, these lower-rated issuers face compressed interest coverage ratios. When combining these upcoming maturity considerations with secular AI workflow disruption, the credit baseline shifts in favor of high yield over loans. High yield bonds are more insulated from these near-term maturity walls and exhibit minimal software concentration risk. Accordingly, our view has shifted away from broad floating-rate loan beta and toward fixed-rate high yield bonds, which offer the opportunity to lock in attractive all-in yields, and we believe the Treasury market may provide an attractive entry point for longer-term investors.

Overall, we continue to expect positive, carry-based total returns for high yield bonds. While spreads remain relatively tight, we view relative valuations as reasonable, given the lower concentration of AI-vulnerable issuers in the high yield market.

Throughout the past three to four months, credit markets have focused intensely on the intermediate- to long-term threat of generative AI to legacy business models, keeping software and business services issuer spreads wider than those for the broader market. While we believe AI will fundamentally affect a range of companies, we also believe the breadth of related sector-wide selling pressure has created attractive total return opportunities in certain instances. Fundamental credit health remains firm; par-weighted default rates ticked up only marginally, staying at a very manageable level relative to long-term historical averages. Ratings activity has trended positively, insulating the benchmark from immediate downgrade stress. Primary issuance has slowed recently, although year-to-date gross volume appears to easily outpace last year’s level. We expect this will be heavily front-loaded, implying more balanced technical conditions for the remainder of the year.

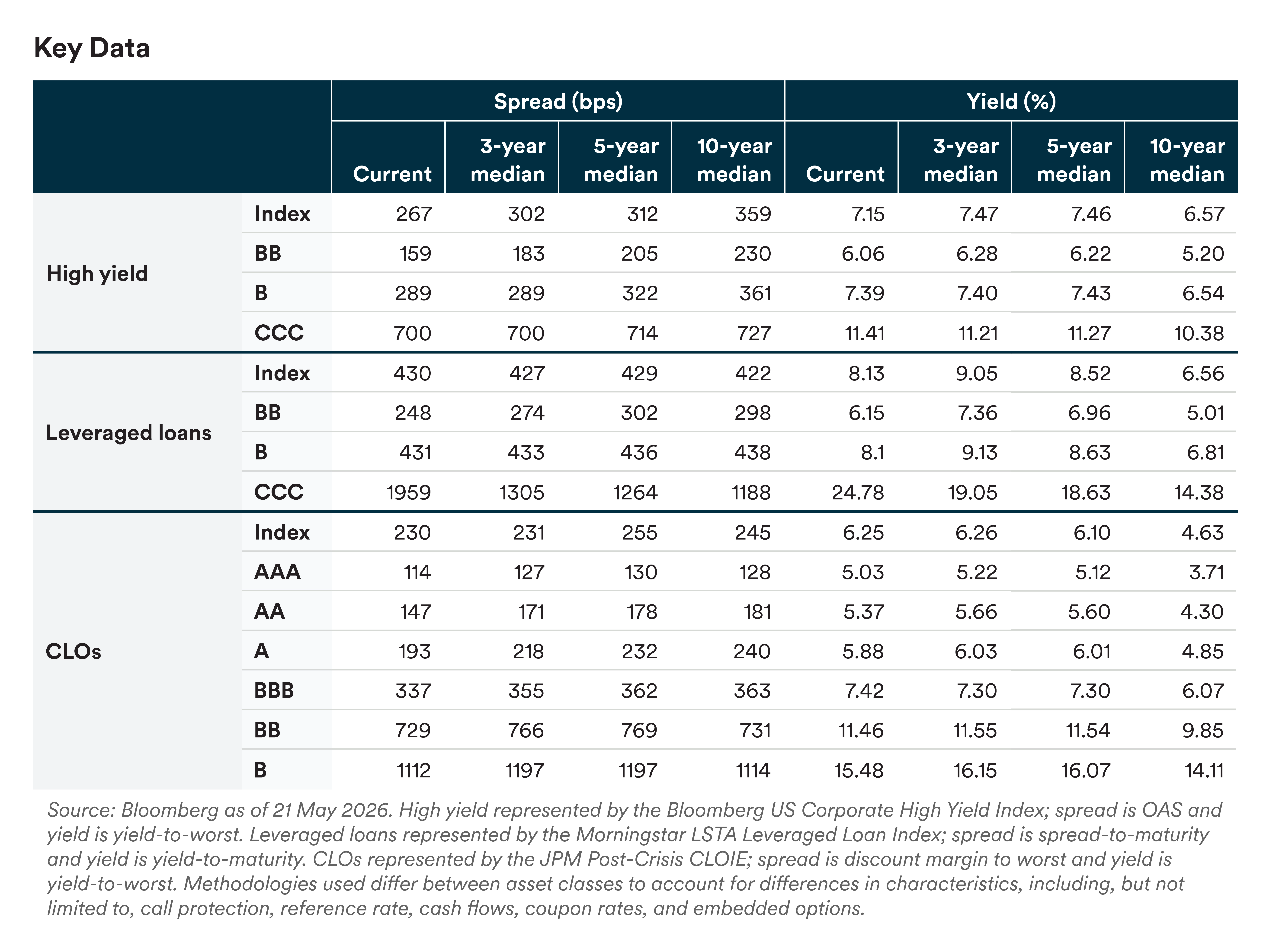

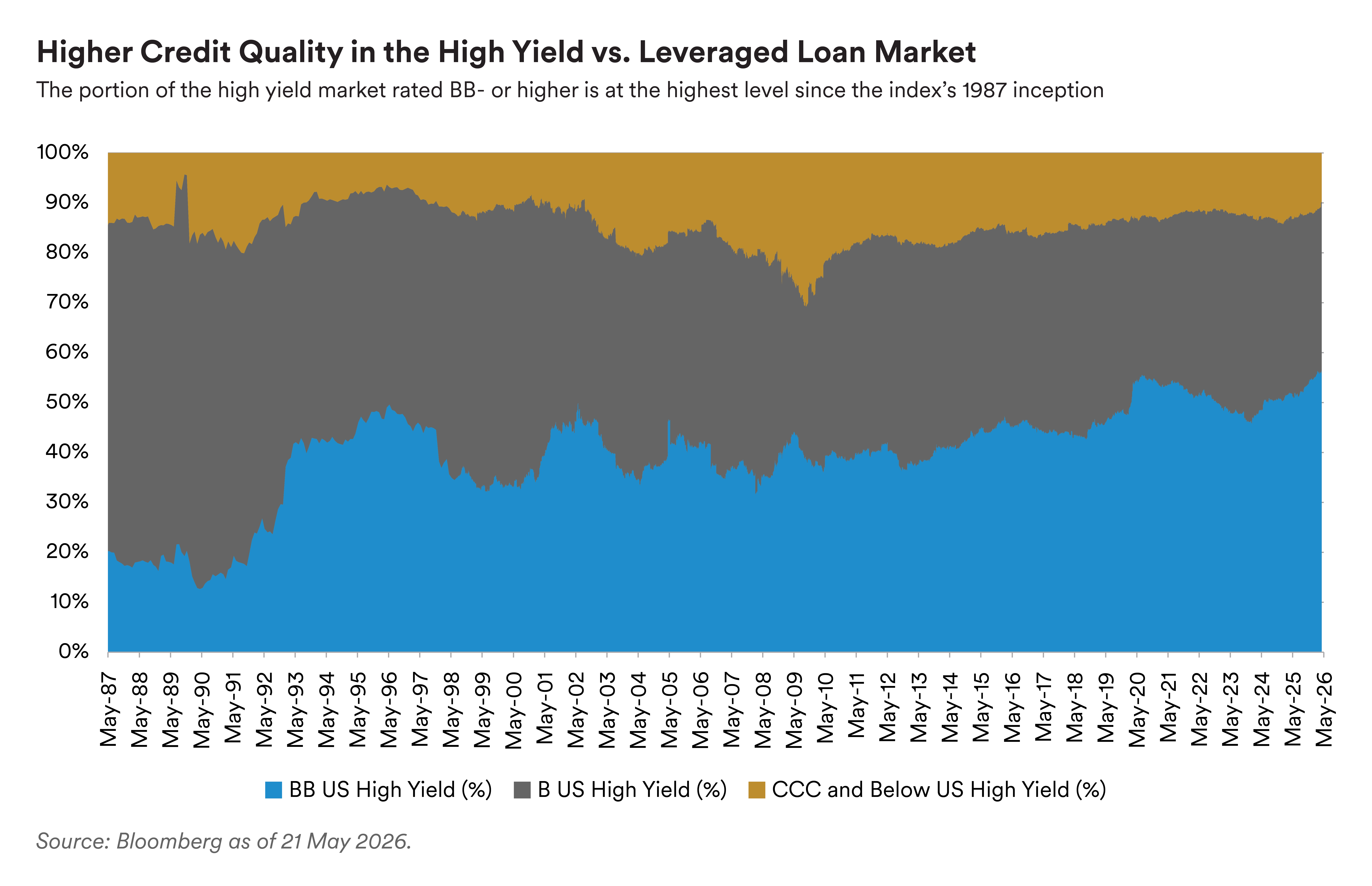

That being said, valuations are tight. The Bloomberg US Corporate High Yield Index spread-to-worst is at 299 (BB 188, B 325, CCC 729), 7 basis points wider year-to-date (as of 21 May), while the yield to worst (YTW) is considerably higher at 7.15%, or 62 basis points higher year-to-date. We see limited scope for a meaningful bull-case spread tightening from these compressed bands; conversely, the primary bear-case catalyst remains a pronounced macroeconomic slowdown or inflationary pressures that accelerate and force the Federal Reserve to begin hiking rates again. However, all-in yields adequately compensate investors for current risks amid low-to-moderate default expectations We continue to view the belly of the high yield market – low-BB to mid-B rated bonds – as a sweet spot for investors: this area avoids the tight spreads in the highest-quality rating tiers along with the default tail risks emerging in the lowest credit segments.

Looking ahead, conditions in the leveraged loan market should remain broadly constructive, but the opportunity set is likely to become more selective as investors balance still-resilient issuer fundamentals against a less certain macro backdrop. As a result, alpha is likely to depend more on disciplined credit selection and downside avoidance than on broad market beta.

Over the coming months, the market’s direction will likely hinge on whether energy-related inflation remains contained, and whether labor market conditions begin to soften more meaningfully. If the current Middle East stalemate persists and commodity price pressure builds, risk appetite could weaken, as higher input costs weigh on margins and consumer demand. Even so, the outlook for performing issuers remains relatively stable for now, supported by several quarters of steady revenue and EBITDA growth and by continued access to capital markets, which should help many companies further reduce interest burdens and extend maturities. AI-related CapEx and government spending should continue to support the economy, absent significant shifts in either driver.

Broadly syndicated loans have higher software exposure, but any AI-related dislocation is likely to emerge gradually and remain concentrated in weaker issuers with near-term maturities that are viewed as lacking AI-resilient business models. More broadly, we do not expect the recent shift in short-term rate expectations to materially change the distress backdrop, as fundamentals remain broadly sound, and performing credits continue to access capital markets to lower borrowing costs and manage maturities, limiting the risk of a sharp rise in distress.

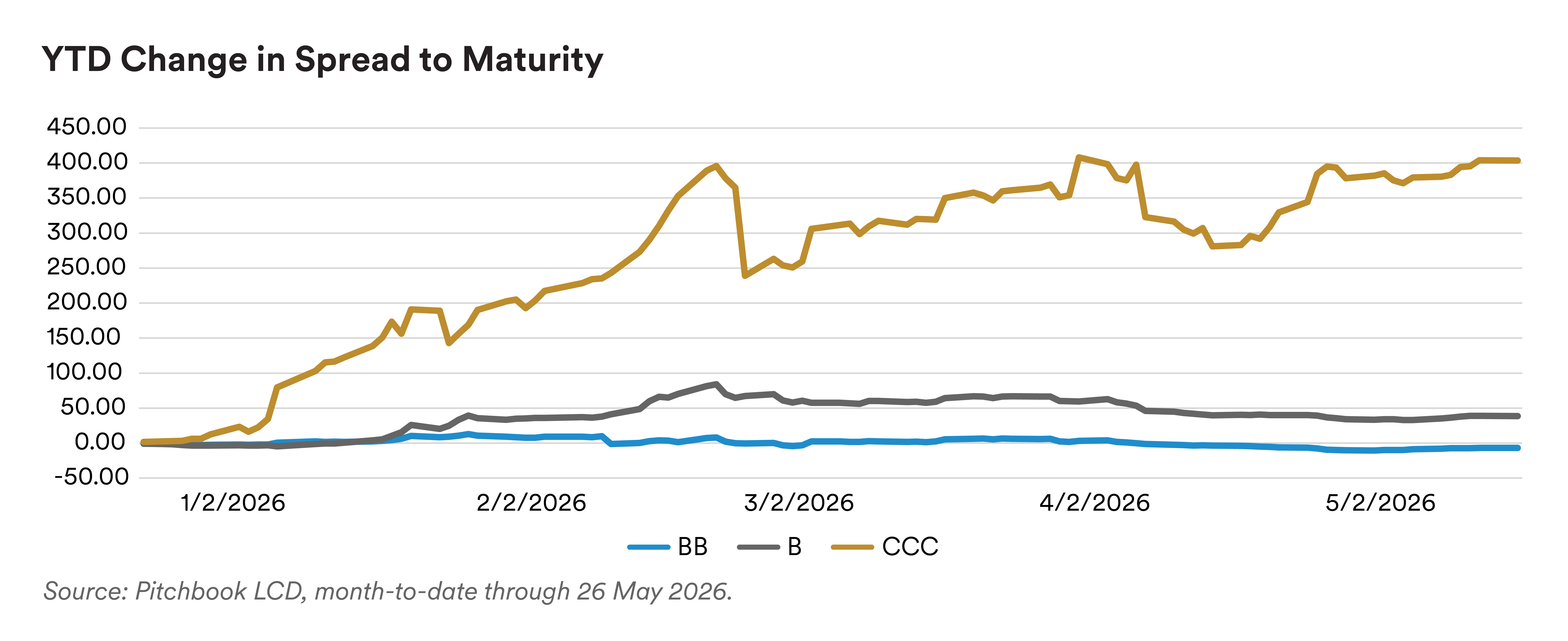

Technicals should remain supportive but are likely to become more balanced from here. A smaller share of the market trading above par should limit repricing activity, while macro uncertainty and rate volatility may keep M&A and LBO issuance subdued. CLO formation should improve further if AAA spreads remain contained, although challenging arbitrage economics for third-party equity could temper the pace of issuance growth. Retail demand is likely to remain tied to headline-driven shifts in sentiment. Higher-quality spreads have remained relatively stable since the beginning of the conflict, while spreads for loans rated CCC have widened amid more pronounced idiosyncratic factors. With near-term rate-cut expectations having receded, all-in yields should remain elevated and provide ongoing support for floating-rate demand, particularly if duration-sensitive assets face renewed pressure.

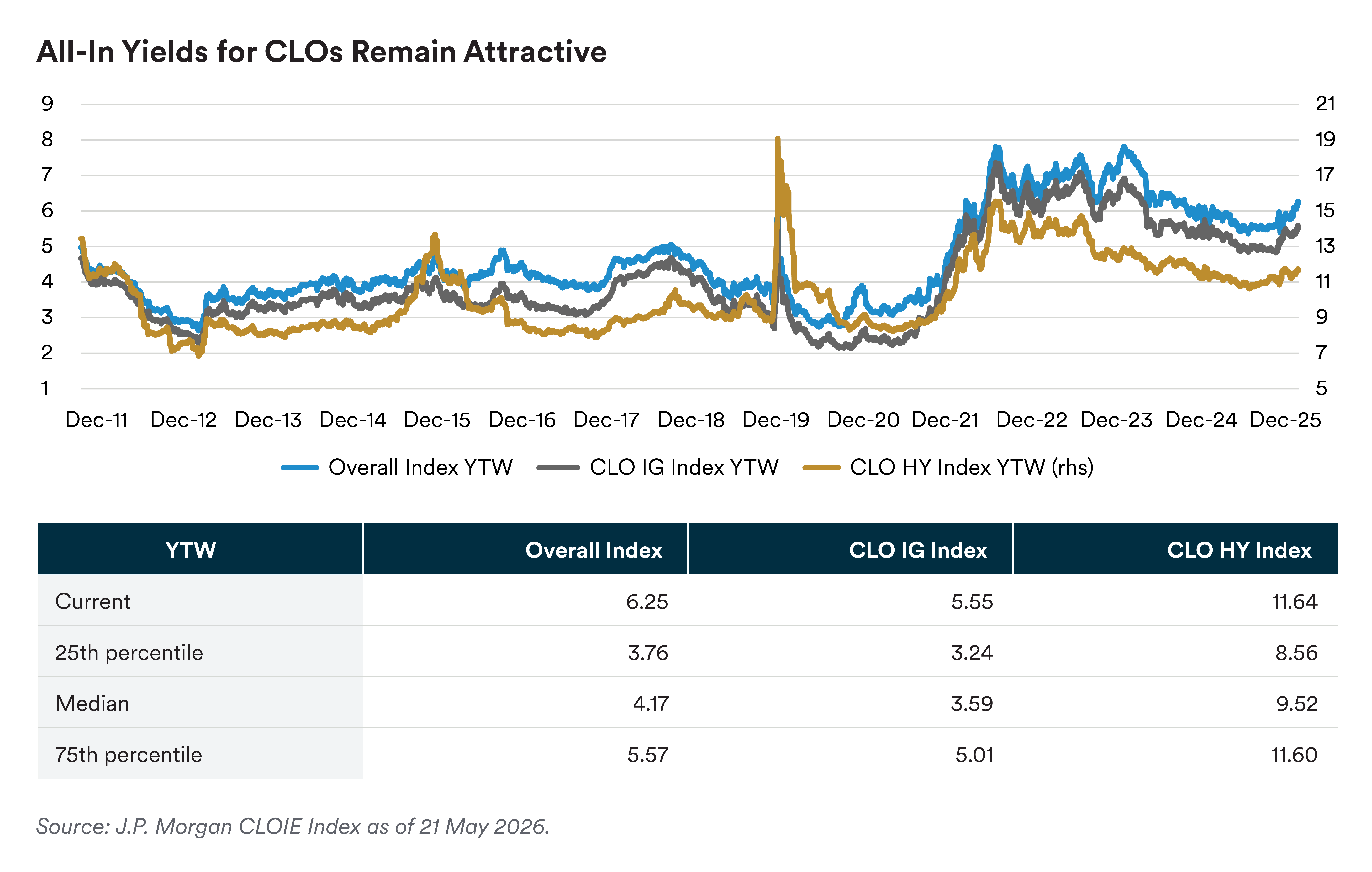

CLO spreads have tightened back to expensive levels, but demand remains strong due to high all-in yields. However, elevated geopolitical risks, persistent inflation and structural challenges like AI-driven disruption are increasing left-tail risks and driving greater dispersion across managers.

Alongside many credit assets, CLO spreads retraced the widening from the end of the first quarter and now appear expensive overall. Despite tight valuations, we anticipate strong demand for CLOs to continue for the rest of the year, particularly for investment-grade tranches. Following three hawkish dissents at the Fed’s April meeting and hotter-than-expected inflation that is expected to remain elevated, given the ongoing conflicts in the Middle East and Ukraine, markets now see a higher likelihood of rate hikes than cuts over the next 12 months. This is a dramatic shift from year-end, when more than two cuts were priced in. As a result, base rates will remain higher for longer, a boon for floating-rate investors, as all-in yields will remain at attractive levels. Against this backdrop, institutional investors have continued to allocate to CLOs, and retail demand has remained robust, with $7 billion of inflows into CLO ETFs, year to date, bringing total ETF assets under management to more than $46 billion.1 In addition, greater clarity on various regulatory regimes — notably, the Basel III Endgame and the NAIC risk-based capital regime — is expected to result in additional demand at the top of the capital stack from banks and insurance companies.

While demand is expected to remain strong, left-tail risk continues to be elevated in CLO portfolios. At a macro level, market valuations appear to be pricing in a near riskless path forward, but the resolution of the conflict in Iran remains elusive, and we anticipate that the impact of the energy price spike should start to filter through into the economy in the months ahead. In addition, while AI fears have taken a backseat following the continuation of the war in Iran, the outcome is likely to have a bigger impact on long-term performance for loan issuers. As a result of AI disintermediation, we continue to see a repricing of risk premia in the form of wider spreads, higher yields and lower prices in software and other AI-impacted credits. In addition, while the chemicals sector has rallied off the lows, long-term systematic pressures remain unresolved. We have seen this play out more acutely in the private credit market, given the asset class’s high exposure to software. While risks in the private credit market are notable, we don’t believe they pose a systemic threat and don’t expect a broader market contagion.

As we have observed increasing tail risks in portfolios throughout 2025 and 2026, we continue to prefer tranche purchases higher in the capital stack. However, select shorter spread-duration assets for lower-rated credits are presenting more opportunistic entry points, amid elevated geopolitical tensions and signs of a K-shaped economy. Despite viewing spreads as tight, we are finding value in AAA, A and junior BBB tranches in the primary market and select equity tranches in the secondary market. We anticipate additional bouts of volatility in the coming months and would like to maintain the ability to shift further into lower-rated tranches during periods of market weakness.

About this Report: This is a quarterly publication which encapsulates insights of the Leveraged Finance Team at PineBridge Investments, a MetLife Investment Management company. Our global team of investment professionals convenes in a live forum to evaluate, debate and establish top-down guidance for the leveraged finance investment universe. Using our independent analysis and research, driven by our Fundamentals, Valuations and Technicals framework, we assess the pulse of high yield, leveraged loans and CLOs.

Endnotes

1 Source: BofA Global Research, Bloomberg, “CLO Factbook,” as of May 15, 2026.

Disclaimer

MetLife Investment Management ("MIM"), which includes PineBridge Investments, is MetLife, Inc.'s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world. The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risk, including possible loss of principal; no guarantee is made that investments will be profitable. This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. Views may be based on third-party data that has not been independently verified. MIM does not approve of or endorse any republication of this material. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

For investors in the U.S.: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities and Exchange Commission (SEC) registered investment adviser. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment adviser.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also sub-delegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees’ pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being distributed by MetLife Investments Asia Limited (“MIAL”), licensed by the Securities and Futures Commission (“SFC”) for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities in Hong Kong S.A.R. This document is intended for professional investors as defined in the Schedule 1 to the SFO and the Securities and Futures (Professional Investor) Rules only. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are licensed by the SFC to carry on regulated activities in Hong Kong S.A.R. The information contained in this document is for information purposes only and it has not been reviewed by the Securities and Futures Commission.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.