In a higher-yield, volatile rate environment, core fixed income once again plays a central role in portfolios. In the current investment environment, core fixed income may provide attractive income, the potential for price appreciation, a focus on capital preservation and a valuable offset to the risk of more volatile assets such as equities. However, we believe that these benefits are best realized by active management that employs a disciplined risk framework to balance exposures among individual credits, sectors and select positioning on the yield curve.

When we think about what makes a successful core fixed income manager, we are inspired by the role of a dependable lead-off hitter in baseball. A home-run hitter may deliver headline-grabbing results, but they may also be inconsistent, generating more strikeouts or walks than a batter that consistently gets on base with singles or even the occasional double. In an active strategy designed to provide stability and take advantage of market dislocations to earn upside, inconsistent performance can make it difficult to deliver long-term outperformance. We think thoughtful manager selection and a keen focus on risk-adjusted returns can help generate robust results across market cycles, just as a reliable lead-off hitter is counted upon to deliver consistent results.

Core fixed income investors have elevated yields and a surprisingly resilient economic backdrop on their side at the moment. The Bloomberg Aggregate Bond Index, a widely used proxy for core fixed income, yielded 4.60% as of April 2026 (Exhibit 1). Higher starting yields not only enhance income potential but also provide a meaningful cushion for capital preservation should volatility re-emerge.

The interest-rate environment remains in flux, but investors should continue to benefit from elevated rates for some time. While the Federal Reserve has reduced the federal funds rate by a cumulative 1.75% over the past two years, bringing the target range to 3.5%–3.75%,1 and labor market data have been deteriorating over the past year, the easing cycle faces headwinds due to inflation and commodity price pressures.

Likewise, core fixed income can play an important role as a diversifier, potentially mitigating risk and making portfolios more resilient. The asset class spans U.S. Treasuries, investment-grade corporate credit, residential and commercial mortgage-backed securities, and asset-backed securities, and within each of those sub-asset classes, investors can find a variety of sectors, issuers and structures.

With attractive all-in yields and a broad opportunity set, core fixed income stands out as a wise allocation for sophisticated investors seeking both capital preservation and yield to enhance portfolio outcomes in 2026 and beyond.

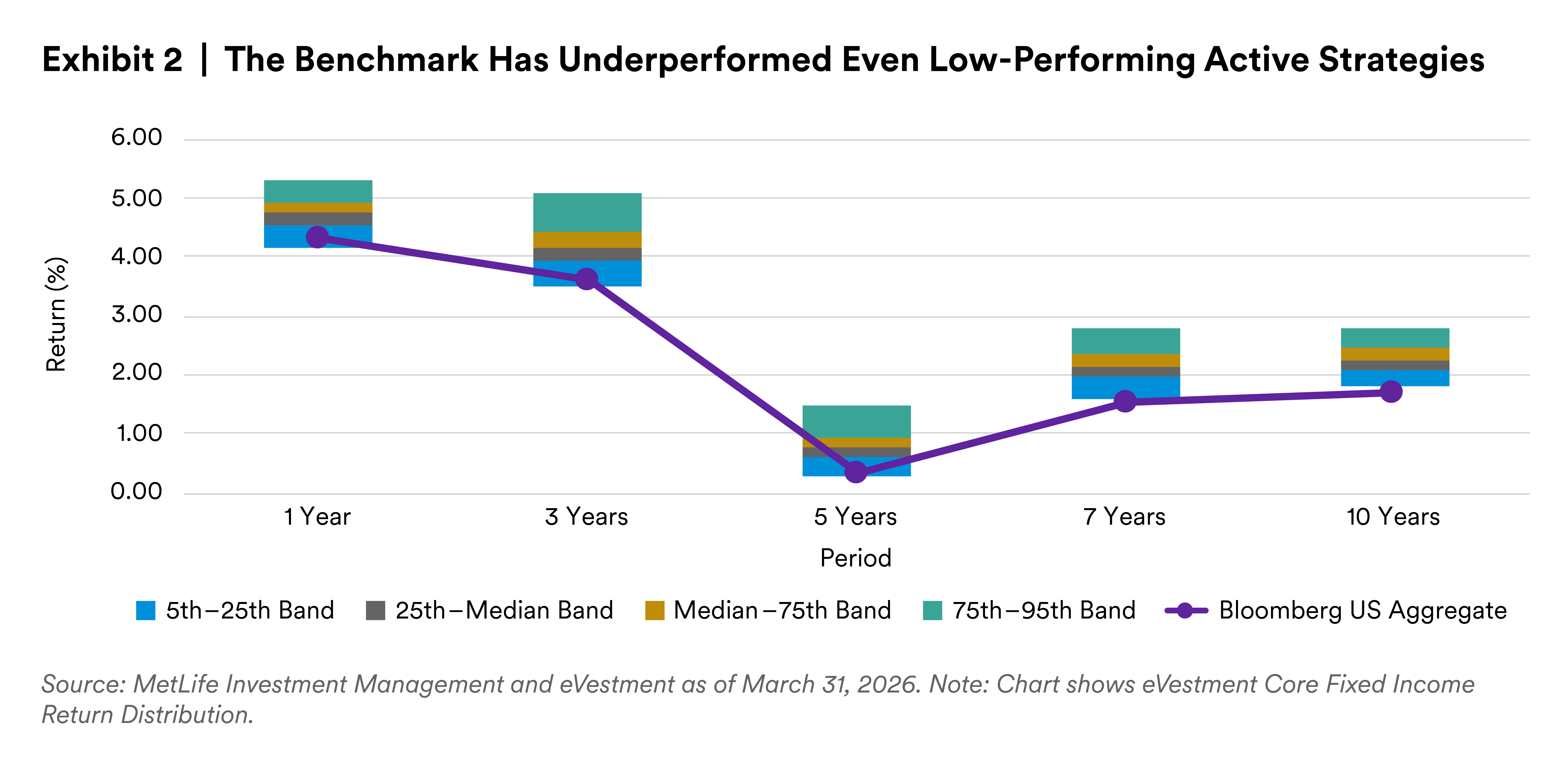

While index strategies such as the Bloomberg U.S. Aggregate Bond Index remain popular, they are inherently constrained by index construction, leading to risk exposures that may not align with investor objectives. That’s because indexes are market weighted, meaning that the more debt an issuer has outstanding, the larger its weight in the index. Indexed allocations can therefore inadvertently expose investors to the most indebted issuers, potentially increasing exposure to less attractive credits or sectors and missing opportunities in off-benchmark securities that do not meet index rules for size, maturity or structure. Index strategy managers are also forced to buy when an issue enters the index and sell when it exits, regardless of valuation, which leaves them unable to take advantage of undervalued securities. From a return perspective, the U.S. Aggregate Index has persistently underperformed active core strategies across both shorter and longer term horizons, ranking below the 90th percentile of its active peers2 across trailing 3-, 5-, 7-, 19- and 20-year performance time horizons (Exhibit 2).

In our view, fixed income markets price interest-rate risk efficiently but regularly misprice securities that are exposed to credit, prepayment, downgrade and liquidity risks. These inefficiencies present a compelling landscape for alpha generation, particularly through disciplined security selection. Active managers are better positioned than passive managers to diversify risk, adjust sector and issuer exposures in real time, and exploit relative value opportunities across the entire fixed income spectrum. Active managers can also draw on a broader opportunity set, such as non-index eligible securities, allowing them to pursue targeted sources of value and adjust risk exposures dynamically. This, in turn, can help avoid risk and reduce exposure to weaker credits that passive indexes must hold.

If security selection is paramount to core fixed income performance, it is important for investors to understand how managers select securities. Balancing security-specific research with an awareness of the overall market environment and existing portfolio exposures is what, in our view, allows an active manager to select securities that are undervalued and avoid those that are cheap for a reason.

Introducing active management does not come without costs, so it is essential to evaluate the benefits of active management through the lens of risk-adjusted returns. In favorable market environments, investors tend to focus narrowly on absolute returns, overlooking the risks taken to achieve those results. However, latent risks often only come to light when markets turn choppy, by which point it is too late to do anything but attempt to limit the damage. Identifying, understanding and proactively managing risk before the tide goes out are a better approach, in our view. Emphasizing risk-adjusted outcomes rather than absolute returns can help ensure that a manager’s returns are not achieved through risk-taking that could ultimately undermine long-term objectives.

And what are those long-term objectives when it comes to core fixed income? We think this asset class should serve as a ballast in a portfolio, offering strong capital preservation potential compared to riskier asset classes, consistent income generation and returns that exceed the benchmark, without deviating into riskier territory in pursuit of higher yields. Even when markets become unsettled, a core fixed income allocation should offer a steady harbor. Risk-adjusted returns allow investors to evaluate whether the returns generated are appropriate for the level of risk assumed. This is a key safeguard, confirming that the investment process is delivering value in a prudent and sustainable manner.

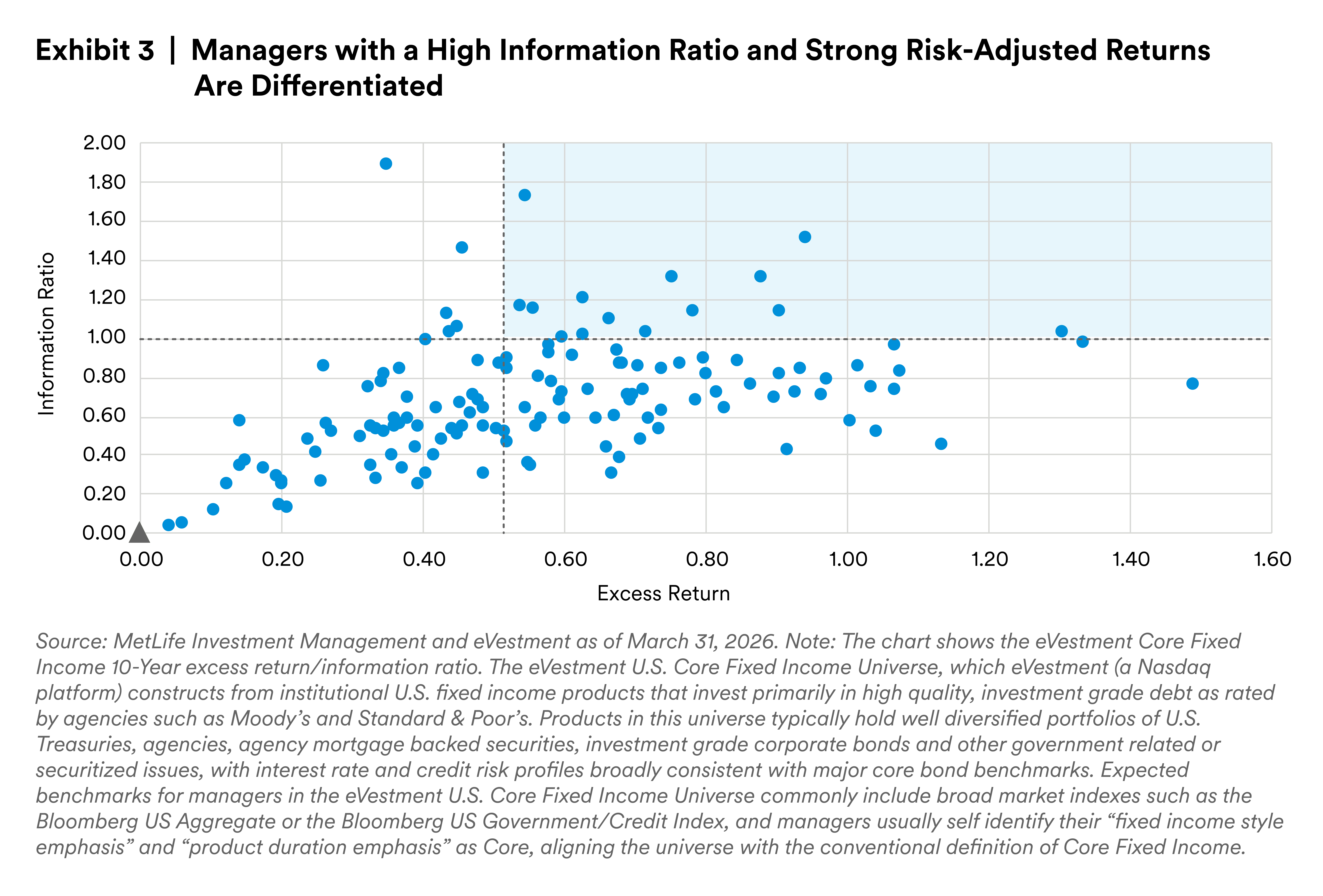

We prefer to compare active core fixed income strategies based on the information ratio (IR), which measures not just the magnitude of excess return over a given benchmark, but also the consistency with which the manager generates that return (Exhibit 3). An investment manager with an information ratio above 1.00 is generally viewed as demonstrating strong and consistent skill, as this level of IR indicates that the manager is generating substantial excess return per unit of active risk taken relative to the benchmark.

Taking a step back, the Fundamental Law of Active Management expresses the IR as the product of the information coefficient, which measures the correlation between a manager’s relative value views and subsequent excess returns, and the square root of breadth, or the number of active decisions a manager makes over time. A manager with a very high information coefficient of 0.5, meaning that their relative value assessments are directionally correct a large majority of the time, would be expected to generate attractive risk-adjusted outcomes even with a relatively modest number of active decisions.

While such a high information coefficient is best viewed as illustrative rather than typical, it does help explain why some managers can sustain high information ratios over time. Plugging an information coefficient of 0.5 into the Fundamental Law, along with moderate active risk and realistic breadth consistent with a diversified core fixed income process, readily produce excess return estimates above 0.5% over a full market cycle.

Core fixed income has a job in a portfolio: It’s meant to provide ballast when riskier asset classes are gyrating, produce healthy income and preserve capital. Skilled managers can also take advantage of price dislocations by finding credits that are truly undervalued and avoiding the large-issuer bias of passive indexes.

Taking undue risk in an allocation designed around stability and preservation, especially at a time when markets are volatile, should have a high cost. The true test of an active manager in core fixed income lies not only in outperformance, but also in a long track record of translating risk into alpha consistently and prudently. Managers who achieve returns by swinging for the fences and taking outsize risks may seem to be at the top of their game when markets are calm. But when macro conditions take a sharp turn or risks related to specific sectors or types of credits emerge, the real cost of those risks can become painfully apparent. Investors should ask how much they’re paying in terms of risk for the returns they can expect to get.

MetLife Investment Management has a 20-year track record of achieving risk-adjusted returns by following a bottom-up process that seeks relative value across the core fixed income universe, evaluates each prospective investment on its own merits, and also accounts for top-down macroeconomic factors and the security’s intended role within the broader portfolio. As a long-tenured management team, we are continually refining our approach, learning from each market event how our philosophy can evolve. However, our approach will stay grounded in thoughtful risk-management and a dedicated team-based culture that insists on active dialogue among portfolio managers, traders, and research.

Endnotes

1 As of April 28, 2026

2 Based on active peers within the Core Fixed Income universe in eVestment. Past performance is no guarantee of future results.

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

MetLife Investment Management (MIM), which includes PineBridge Investments, is MetLife Inc.’s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world.

This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

For investors in the U.S.: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities and Exchange Commission (SEC) registered investment adviser. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment adviser.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a "professional client" as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also sub-delegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees' pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being distributed by MetLife Investments Asia Limited (“MIAL”), licensed by the Securities and Futures Commission (“SFC”) for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities in Hong Kong S.A.R. This document is intended for professional investors as defined in the Schedule 1 to the SFO and the Securities and Futures (Professional Investor) Rules only. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are licensed by the SFC to carry on regulated activities in Hong Kong S.A.R. The information contained in this document is for information purposes only and it has not been reviewed by the Securities and Futures Commission.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.