Six months into the year, the message from our January outlook still largely holds: stay calm, stay invested and focus on diversified yield and carry rather than reaching for outsized excess returns. What has changed is the backdrop. Fixed income markets have absorbed a sharp reset higher in rate expectations, a new geopolitical shock in the Middle East and a resurgence of inflation concerns, yet spreads across many sectors have retraced much of their widening and are again trading at tight levels. In our view, that resilience continues to reflect the importance of carry, steady technical demand and fundamentals that remain generally intact, even as valuations leave less room for error.

Our core view remains constructive and selective. All-in yields continue to support fixed income, and fundamentals across much of investment grade credit, leveraged finance, CLOs and emerging markets remain reasonably sound. Valuations leave less room for error; market differentiation has narrowed; and investors are increasingly being paid for carry rather than for taking broad directional credit risk. In that environment, we believe portfolios should remain invested, while emphasizing security selection, diversification and dry powder to deploy during bouts of volatility.

Carry is still doing the heavy lifting. Across investment grade (IG), leveraged finance, CLOs and emerging markets, higher all-in yields have kept demand firm even as spreads sit near tights, and macro risks have risen.

Valuations now require more selectivity. We continue to see opportunities, but broad beta looks less compelling than it did earlier in the year, and issuer, sector and regional selection matter more.

AI is increasingly reshaping credit markets. It is changing index composition, issuance patterns and relative value across investment grade and leveraged finance, creating both opportunities and pockets of risk.

The key risk is that tight spreads leave less room for surprise — including persistent inflation, elevated energy prices and the possibility of central bank policy error — but markets have so far absorbed major shocks, while maintaining support from income-oriented demand.

Several assumptions behind our original outlook have been tested since January. Inflation expectations have moved higher; the path for the Federal Reserve has reset; and the conflict in the Middle East has lifted energy prices and added another layer of geopolitical uncertainty. Even so, credit markets have remained resilient. Spreads widened during the March-April sell-off, but many assets have since retraced that move and now sit close to local tights. In our view, that speaks to a market still dominated by yield buyers and supported by fundamentals that have not meaningfully deteriorated.

That leaves us constructive, while still mindful of broad market valuations. We believe fixed income can continue to deliver positive, carry-based returns, and we do not view recent stresses in private credit and software or idiosyncratic credit events as evidence of an imminent systemic blowup. The market is broadly pricing in a continuation of the current mix: Geopolitical uncertainty that remains contained; inflation that does not reaccelerate meaningfully; and growth that stays intact. If that path changes, tight spreads offer limited cushion, making selectivity important.

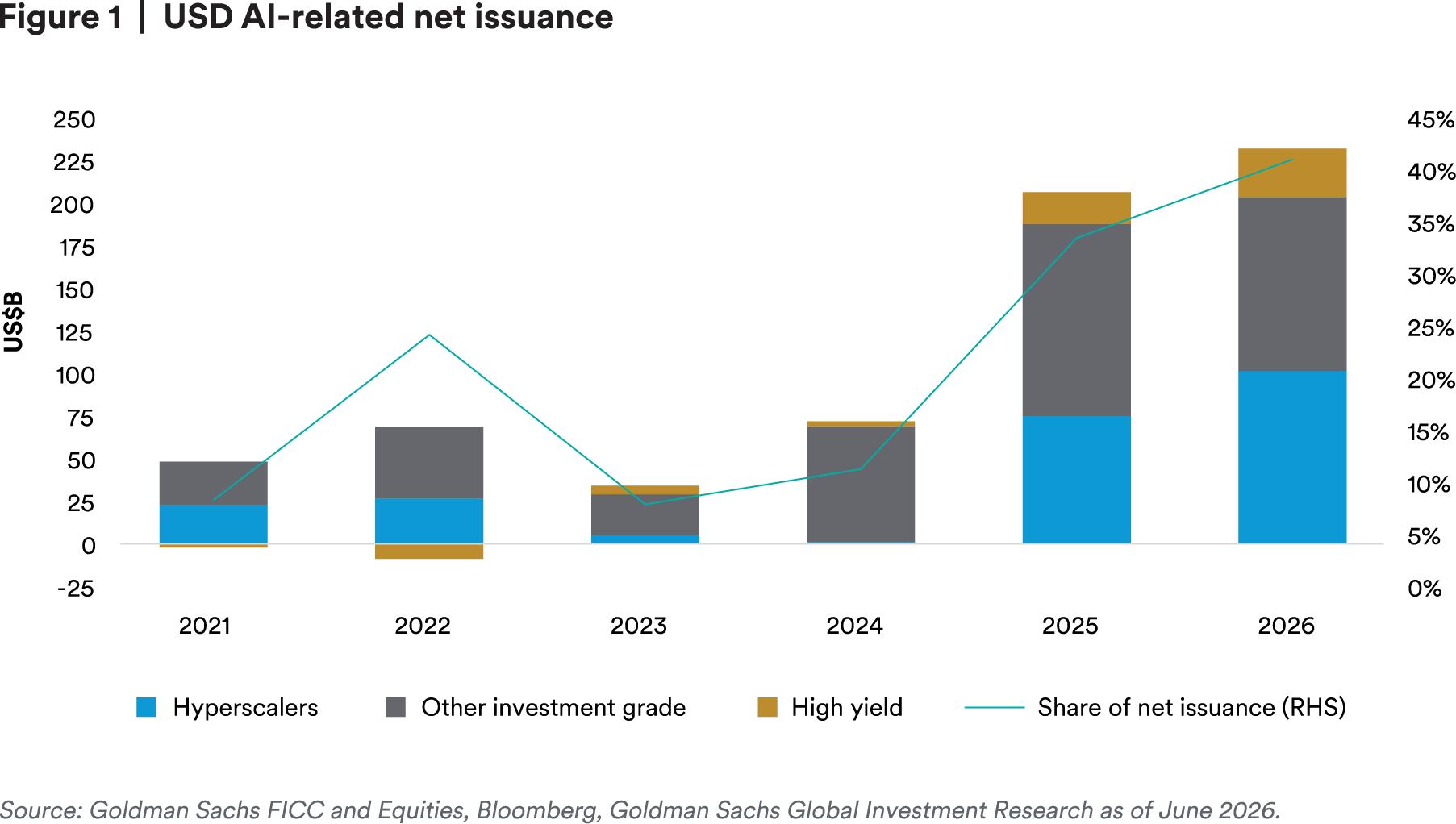

In IG, the first half of the year has reinforced a key point from our prior outlook: Technicals remain in the driver’s seat. Issuance rose sharply, helped by AI-related hyperscaler financing as well as M&A, corporate spin-offs and recapitalization activity. Yet the rise in Treasury yields reset all-in yields higher and kept demand robust. That push-pull between spread and yield has so far been won by yield.

AI is also having a more direct effect on the investment grade market than many expected in January. Companies with some of the strongest balance sheets in the market are now issuing debt to finance AI and data-center build-outs, increasing the weight of large, high-quality technology issuers in the index. That has improved index quality in some respects, but it has also changed market composition and introduced new questions around concentration, correlation with equities and how to value debt financing structures tied to AI infrastructure.

We also see a notable level of homogeneity in IG, with not a lot of issuer differentiation. This underscores our emphasis on seeking the best companies within sectors rather than relying on broad market exposure. Over time, we expect risk and spreads to become more differentiated, and we think it is critical to be positioned on the right side of that dynamic. We continue to favor intermediate investment grade credit over the long end and continue to seek exposure to the best companies.

Our leveraged finance view also remains broadly intact, though our relative preferences within the asset class have become clearer. We remain constructive on both high yield bonds and leveraged loans because yields continue to compensate investors reasonably well, and default expectations remain manageable. But we currently favor fixed-rate high yield over floating-rate loans. Loans still look optically inexpensive in places, but much of that apparent value reflects market composition. The loan market remains much more exposed to software, while high yield has greater exposure to areas such as energy that have held up better in the current environment.

The AI divide is becoming increasingly important here. In leveraged finance, the most direct beneficiaries are the “picks and shovels” of the theme — hardware, power, utility and data center-related issuers — while software and certain tech-enabled business models face more pressure as investors reassess business-model durability. That divergence is also feeding through to CLOs, where strong demand and elevated all-in yields continue to support spreads, but left-tail risks are rising, and manager selection matters more. We still see attractive carry in higher parts of the CLO capital stack and believe a nimble approach is essential if market weakness creates opportunities lower down.

More broadly, we still expect carry-based returns rather than large spread compression. In high yield, we continue to prefer the belly of the market — low-BB to mid-B rated bonds — where investors can avoid both the very tight spreads in the highest-quality tiers and the more acute default risk at the bottom of the capital structure. In loans and CLOs, we think disciplined bottom-up credit work and downside avoidance will matter more than broad beta exposure as markets become more selective.

Emerging markets (EM) have also held up better than many might have expected, given the rise in oil prices, renewed inflation worries and uncertainty around the Strait of Hormuz. The broad story remains supportive: Many EM countries still enter this period with stronger policy credibility, healthier balance sheets and more attractive real-rate profiles than their developed-market peers. That continues to argue for a strategic role for EM debt, particularly as a diversified source of yield and carry.

That said, the easy relative-value trade has become less obvious. The widening in March and April has largely been reversed, and the distinction between oil exporters and importers has narrowed much faster than expected. Investors searching for income have been willing to move down the quality spectrum despite macro noise, which has compressed spreads even in countries still exposed to elevated energy prices.

As a result, we think the opportunity set in EM is becoming more idiosyncratic. We believe EM corporates continue to add value relative to other areas and see value in selective local-currency exposures in higher real-rate markets and in parts of the single-B universe, while remaining mindful of inflation-sensitive areas such as high-quality Asia. Elections in countries such as Brazil and Colombia also warrant attention as potential drivers of sentiment and volatility in the second half.

At midyear, the central tension in fixed income is straightforward: Valuations imply a fair amount of good news, while the macro backdrop still contains meaningful uncertainty and risk. This is a subtle but important tension: The bullish case is less that fundamentals are great and more that income is compelling enough to overwhelm concerns. That makes the market more vulnerable if yields fall, recession fears rise, or risk appetite changes.

Elevated energy prices, higher food costs and tighter financial conditions could weigh on the consumer and slow growth in the back half of the year. At the same time, there is a real risk that central banks respond too aggressively to what ultimately proves to be a temporary inflation impulse. Either outcome would challenge a market that has been quick to buy dips and slow to sustain wider spreads.

Even so, we continue to view fixed income as attractive in a world where income is scarce, and uncertainty is high. We still believe investors should stay calm and keep their carry on — but with a more selective, diversified and valuation-aware posture. That means favoring quality where appropriate, leaning into areas where market composition has created better relative value, and keeping enough liquidity to respond when volatility creates more compelling entry points.

Disclosure

MetLife Investment Management ("MIM"), which includes PineBridge Investments, is MetLife, Inc.'s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world. The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risk, including possible loss of principal; no guarantee is made that investments will be profitable. This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. Views may be based on third-party data that has not been independently verified. MIM does not approve of or endorse any republication of this material. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

For investors in the U.S.: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities and Exchange Commission (SEC) registered investment adviser. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment adviser.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also sub-delegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees’ pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being distributed by MetLife Investments Asia Limited (“MIAL”), licensed by the Securities and Futures Commission (“SFC”) for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities in Hong Kong S.A.R. This document is intended for professional investors as defined in the Schedule 1 to the SFO and the Securities and Futures (Professional Investor) Rules only. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are licensed by the SFC to carry on regulated activities in Hong Kong S.A.R. The information contained in this document is for information purposes only and it has not been reviewed by the Securities and Futures Commission.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.