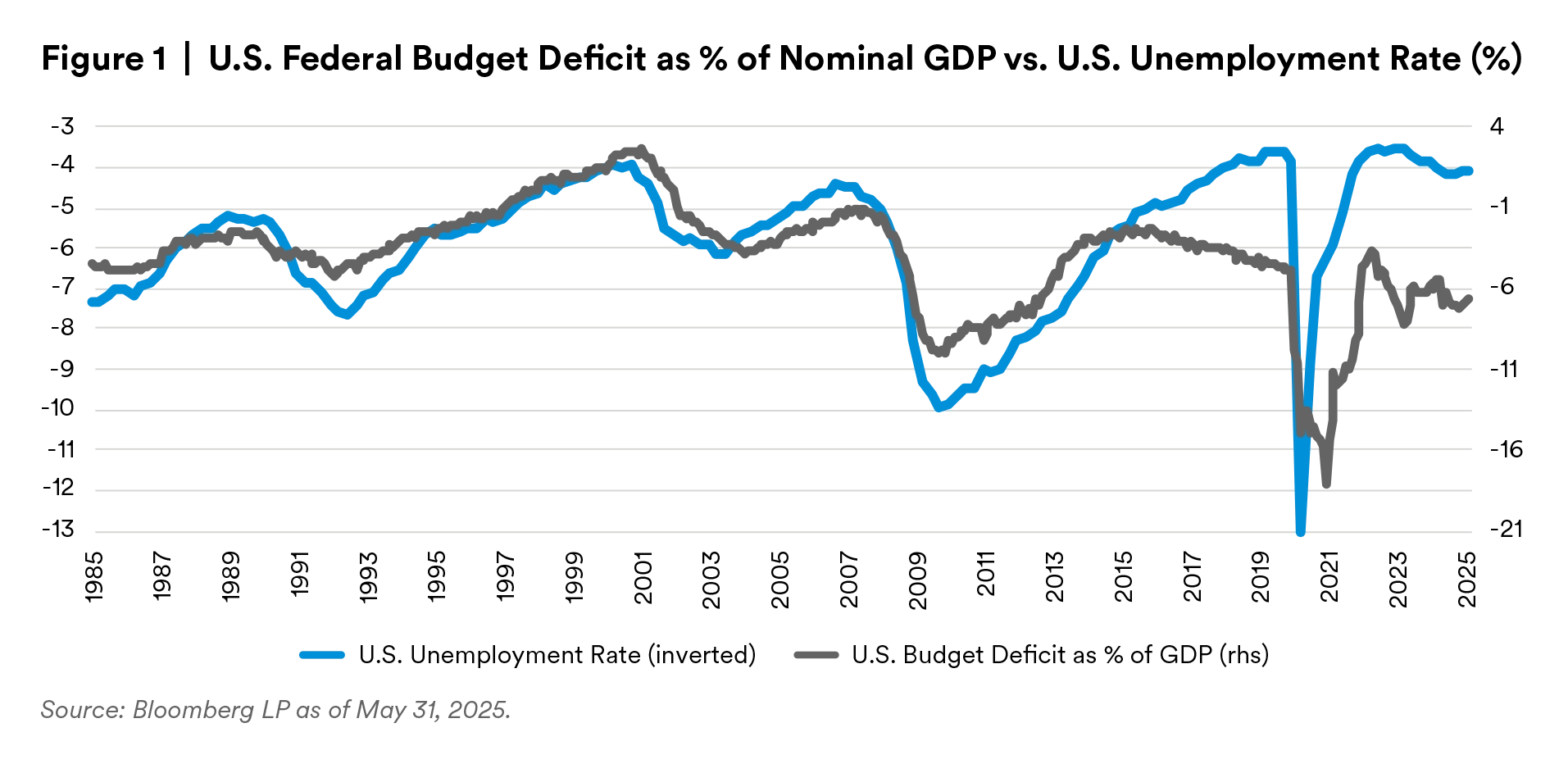

At present, the U.S. growth outlook is being stifled by new and evolving secular forces including the limitations of deficit-financed growth policies, increasing tariff rates and declining rates of immigration. The combined effect means that U.S. growth is more likely to slow, converging toward other Developed Market (DM) economies once the full effects of these policies are reflected in the economic data. The chart below illustrates a concerning and unsustainable dynamic: Sustained high federal deficits have become decoupled from declining unemployment, suggesting that the period of pro-cyclical fiscal impulse has reached its limitations. This, combined with increasing tariff rates and reducing immigration initiatives, points in the direction of a slower growth rate in the U.S. as these changes are digested. In such scenarios, the U.S. dollar often weakens, reducing the debt burden for EM countries that have borrowed in dollars and making their assets more attractive. Enhancement of unilateral trade relations, stabilizing commodity prices and ongoing structural reforms within EM economies can further enhance EMD’s relative appeal during these periods.

EMD has been generally underowned by investors in recent years, as asset allocators have maintained an underweight due to the asset class's underlying complexities. This gap in ownership, coupled with improving fundamentals, creates a potentially favorable environment for capital inflows. Additionally, the potential for a weaker U.S. dollar in 2025 could further support inflows into local currency-denominated debt and more dynamic hard currency funds. With supply remaining subdued, P&I payments remaining high, and crossover investors increasing allocations to the asset class, issuers across the ratings spectrum have maintained market access or are in the process of regaining it, offering potential down-in-quality convergence and attractive new issue premiums.

The EM sovereign space offers investors a liquid option to diversify away from DM. It provides the potential for additional spread pickup, historically strong returns through cycles and the opportunity for more duration in high-yield assets. DM sovereigns are experiencing challenged fundamentals, lower growth rates and uncertain defense spending; meanwhile, EM economies are demonstrating stronger fiscal discipline and enhanced monetary policy frameworks. Based on a recent study conducted by our sovereign analysts evaluating current fundamentals, 68 of the 81 EM countries (84%) have stable or improving ratings trajectories over the next two to three years. We also see the potential for six to eight countries to be Rising Stars over the next two to three years, given positive momentum. Given this analysis, we believe improving sovereign fundamentals, coupled with the supportive technicals backdrop, will help generate positive spread returns over the near term.

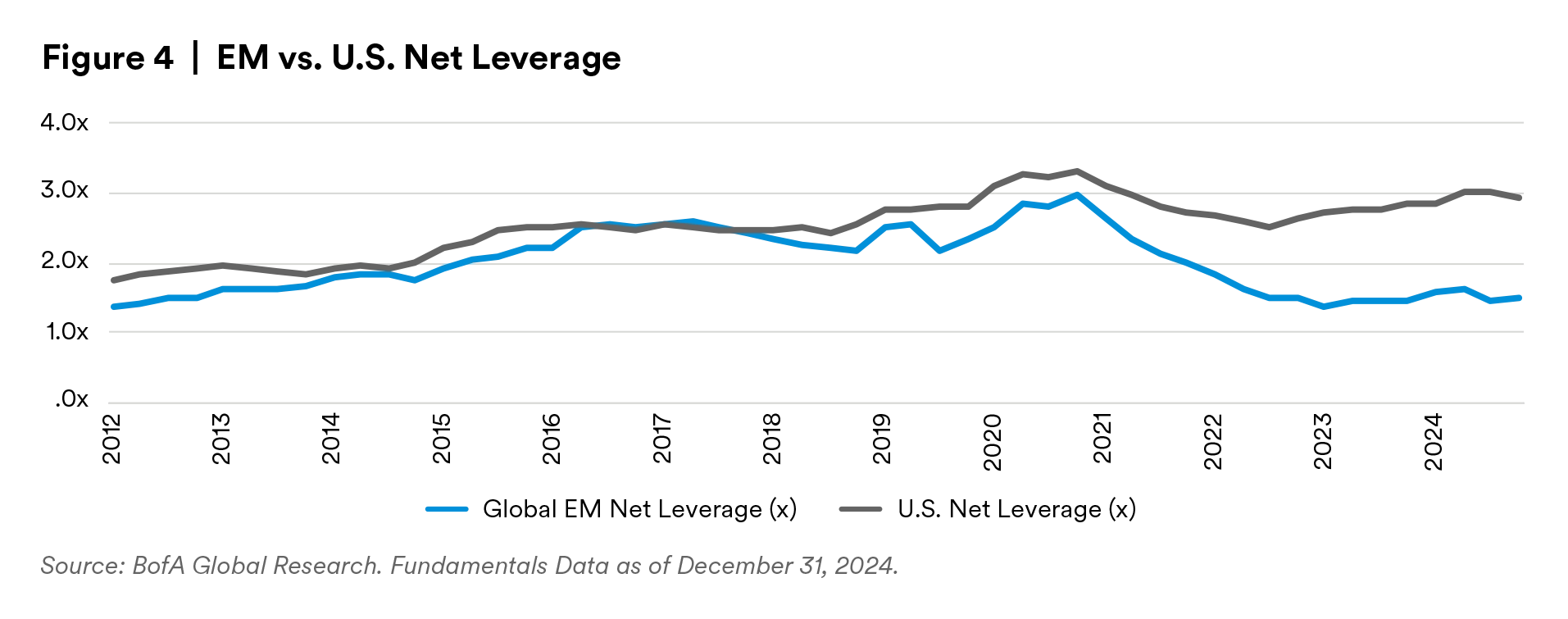

Strong fundamentals also continue to be a theme among EM corporates, and the space provides potential opportunities to invest in stable companies with strong cash flows across the globe, at an attractive pickup over DM corporates. Therefore, despite EM valuations toward the tighter end of the historical range, EM corporate fundamentals remain durable. Positively, spread-per-turn of leverage continues to screen attractive across EM assets and remaining over double, 44 bps/x for U.S. credit versus 114 bps/x for Global EM1 . Additionally, since the Global Financial Crisis, EM defaults have been on average lower than within DM.

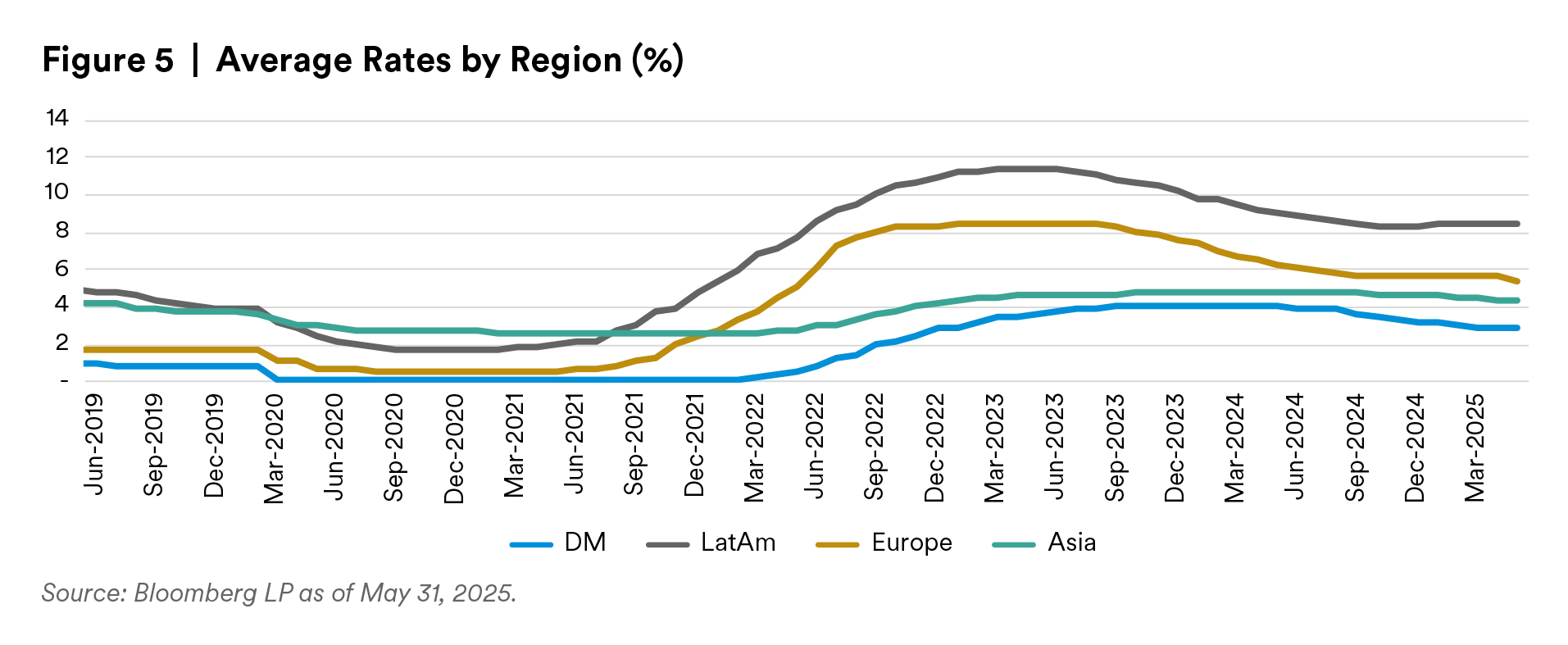

While we understand that the local currency portion of the market has underperformed in recent years due to the strong dollar environment, if investors can buy into the U.S. slowdown story, the case for a weak dollar and therefore supportive backdrop for EM local can be made. Considering elevated dollar valuations over the previous several years, we believe that the U.S., with more constrained fiscal policy and potentially higher inflation, will have lower growth and lower real rates, therefore challenging the dollar’s longstanding outperformance. EM countries have managed to keep inflation under control more effectively than DM, partly due to more measured fiscal and monetary responses to the COVID-19 pandemic. This has resulted in lower inflation rates and reduced pressure on central banks, allowing for more accommodative monetary policies and enhancing the attractiveness of local currency debt. This has also allowed for appealing real rates in many EM countries, providing opportunities in the space as the narrative shifts.

It should be no shock to investors that EM securities typically have a higher beta response to global events, ranging from the trade war in 2016, COVID-19 and its aftereffects in 2020, and in 2022 following the Russia/Ukraine war. From both an excess return and risk-adjusted return perspective versus other asset classes, EM assets have performed well through market cycles, often offering attractive opportunities to investors. EM excess returns have tended to outperform U.S. markets, notably in the investment-grade space, during these periods of shock to the markets. Further, investors generally are compensated for the additional risk they may take in EM, with a historically higher return-per-unit of risk versus the U.S. market.

EMD offers the potential a combination of diversification, yield potential and resilience, making it a compelling option for investors seeking to navigate shifting global economic landscapes. Across sovereign, corporate and local debt, the asset class provides potential opportunities to leverage improving fundamentals, favorable technicals and attractive valuations — especially in an era when DM faces increasing headwinds.

Endnote

1 Source: BofA Global Research. Fundamentals data as of 12/31/2024, Spreads data as of 5/31/2025.

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets.

For investors in the U.S: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment advisor.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also sub-delegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees’ pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being distributed by MetLife Investments Asia Limited (“MIAL”), licensed by the Securities and Futures Commission (“SFC”) for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities in Hong Kong S.A.R. This document is intended for professional investors as defined in the Schedule 1 to the SFO and the Securities and Futures (Professional Investor) Rules only. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are licensed by the SFC to carry on regulated activities in Hong Kong S.A.R. The information contained in this document is for information purposes only and it has not been reviewed by the Securities and Futures Commission.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.

1 As of March 31, 2025, subsidiaries of MetLife, Inc. that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors include Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Investment Management Japan, Ltd., MIM I LLC, MetLife Investment Management Europe Limited and Affirmative Investment Management Partners Limited.