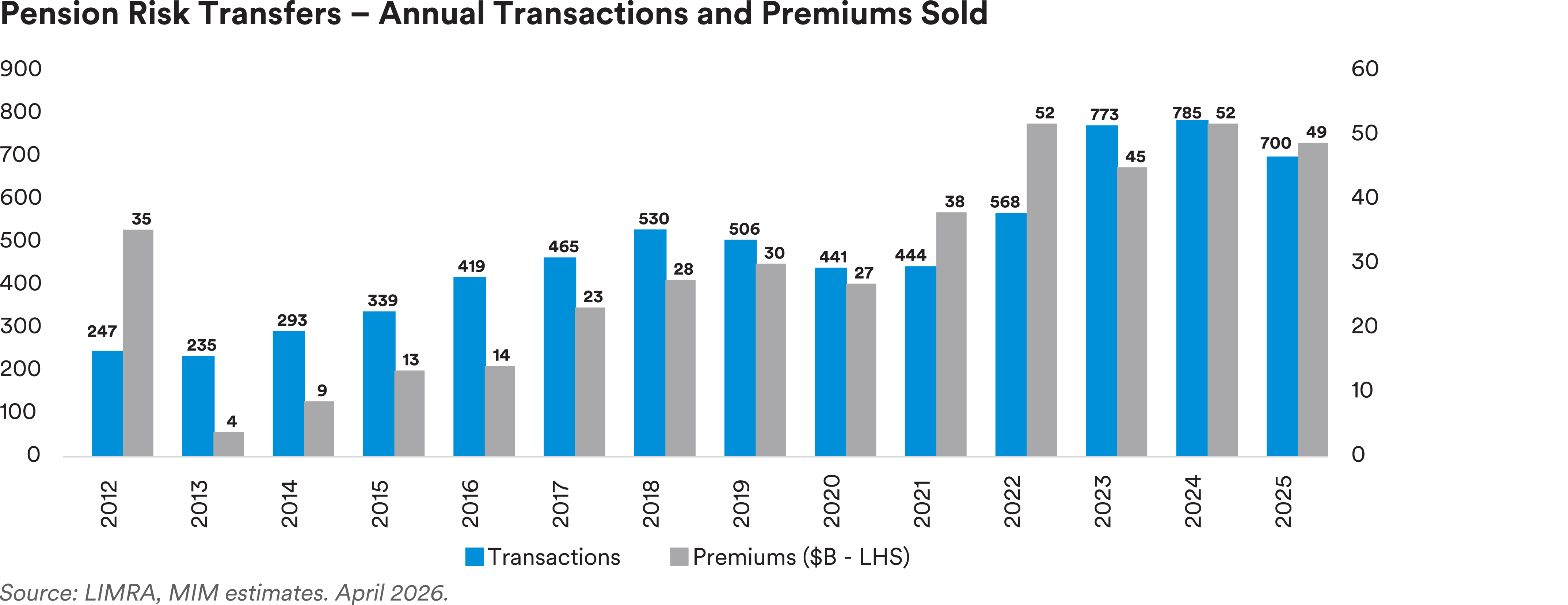

Annuity purchases are popular and effective ways for U.S. corporate pensions to derisk balance sheets through a pension risk transfer (PRT). The average corporate pension has been fully funded since 2022, and plans have taken advantage of their improved funded status and higher interest rates to engage in record levels of PRTs.

In this era of full funding, sponsors tend to have one of three goals: termination, hibernation or continuing to grow plan surplus.1 Retiree lift-outs, a type of PRT, can potentially help with all three, and many plan sponsors have already conducted one or more. In fact, while plan terminations account for most of the PRT transactions, because of their larger size, lift-outs account for the majority of PRT premiums.

Lift-outs alter pension economics, accounting results and hedging effectiveness. Understanding the trade-offs can help manage these impacts.

When considering which participants to include in a lift-out, retirees with small benefits are usually at the top of the list. The inclusion of small annuitants, such as those receiving less than $180/month,2 are compelling because plans pay the PBGC an annual flat rate premium for each participant regardless of the value of their benefit. The 2026 premium is $111 and future premiums are indexed to national average wage growth.

The net effect of removing retirees with small pensions is an improvement in expected future funding level. Eliminating the flat rate PBGC premium for small annuitants tends to outweigh the potential investment upside on the assets used to fund the lift-out.

However, the accounting impact of a lift-out is negative. Pension accounting income is the difference between expected asset returns and expected liability growth. Most plans expect assets to grow faster than their liabilities. The average expected return on assets in 2026 is 6.44% and the average discount rate is 5.37%.3

For lift-outs, the premium paid is generally very close to the accounting liability. So, for accounting purposes, plan surplus or deficit is largely unchanged.4 Yet, because assets are assumed to grow faster than liabilities, lift-outs decrease pension income.

Lift-outs change pension liabilities in ways that make hedging more difficult. To show why, we created a model in which retirees represent half of the plan prior to the PRT and have an average duration of eight years. We assume all retirees are included in the lift-out and that the remaining participants have a duration of 15 years. The average duration for the plan is 11.5 years. (A typical lift-out may not include all retirees.)

After the lift-out, liabilities have a longer duration (15 years vs. 11.5 years), making the plan more sensitive to interest rate movements. Likewise, removing retirees shifts the liability cash flow profile toward longer maturities. This results in a higher liability discount rate spread (0.87 to 1.01%). Consequently, the plan’s remaining liabilities become more exposed to moves in both interest rates and credit spreads.

Pension plan sponsors can use liability-driven investing (LDI) assets to pay for a lift-out. These are referred to as asset-in-kind (AIK) purchases. AIKs provide insurers with liquid assets that may match well with the liabilities, reducing risk for the insurer.5

However, LDI assets are often long-duration bonds, which typically match retained pensions better than those in a retiree lift-out. If used in an AIK, the plan’s asset hedge is often reduced significantly.

Finally, when publicly traded bonds or other liquid assets are used to pay for retiree lift-outs, illiquid assets will represent a larger proportion of total plan assets and may exceed plan investment policy limits.

The example in the table below incorporates some elements of a recent jumbo PRT, a partial lift-out annuitizing retirees with smaller benefits. Our example assumes the transaction was funded with long-duration bonds. As the table shows, the plan’s allocation to alternatives increased, while the hedge ratio decreased.

Thoughtful planning can improve post-lift-out hedging. For example, other liquid assets like equities can be used instead of long-duration bonds. Using bonds that better match the retiree payout profile, like intermediate-duration bonds, might be beneficial to both the insurer and the plan. Finally, the annuity provider may be willing to accept some illiquid assets as part of the AIK. Hedging can also be managed after the lift-out, for example, with the use of an LDI overlay to help maintain the desired hedge.

We expect that the conditions that have supported historically high levels of PRTs will continue. Retiree lift-outs can benefit plan sponsors who want to eventually terminate a pension, hibernate the plan or grow pension surplus.

However, pension balance sheets look different after a lift-out. Lifting out retirees who receive small pensions, a common approach, improves future funded status. However, it also tends to reduce pension income and make remaining plan liabilities more vulnerable to interest rate and spread volatility. With an AIK, plan assets may become less effective hedges and less liquid.

Sponsors who anticipate and manage changes during a lift-out can address many of these issues. Effective plan management, modeling the included group appropriately and making informed choices about which assets to use in the purchase can potentially reduce volatility and optimize plan economics.

Our illustrative plans are hypothetical, have $1 billion in liability, are frozen and have no unrecognized gain/loss. Each has a typical maturity, with retirees representing half of the plan. The PRT in each case annuitizes the retirees, and the PRT premium is equal to the balance sheet liability, i.e., 100% of projected benefit obligation (PBO). Asset allocation is less risky for higher funded status examples. The expected risk premium is 463 basis points.

Plan specifics may cause different results. For example, exceptions include plans where assets have a lower expected return than the discount rate, plans with large, unrecognized gains where shrinking the plan would accelerate recognition and transactions at a significant discount to PBO. These exceptions are believed to be rare.

Endnotes

1 Pension hibernation means a fully funded and fully derisked pension where assets are managed in a way that preserves pension funded status. Pension hibernation means a fully funded and fully derisked pension where assets are managed in a way that preserves pension funded status. There have been discussions about reopening pensions, like the IBM announcement in late 2022. However, most large corporate pensions remain frozen. MetLife’s 2025 Pension Risk Transfer Poll reports that 80% of respondents with derisking goals plan to fully divest their pension liabilities within the next five years. Aon, in their 2025 Global Pension Risk Survey – U.S. Findings, reports that 68% of respondents report a long-term objective other than plan termination.

2 Our estimate of the breakeven level is $180 per month using current mortality, interest rates and PBGC premiums, expected returns on invested assets and 2026 discount rates. Below this level, plan savings on annual flat rate PBGC premiums are greater than the expected excess return on assets associated with retaining the pensioners in plan. Specifics will vary by plan.

3 The average discount rate and expected return on assets assumptions were determined using data provided by Bloomberg and based on the most recent SEC Form 10-K filings as of March 31, 2026 for Russell 3000 companies with pensions and removing outliers, e.g., discount rates below 4.25% and expected returns on assets greater than 9%. Liabilities will also grow with service cost, if any. Pension income may also include amortization of previously deferred items.

4 Lift-outs generally do not impact plan surplus or deficit in a significant way when only retirees are included in the covered group. However, funded ratio will change as this surplus or deficit is divided across a smaller plan, i.e., a denominator effect.

5 In AIK transactions, bonds often comprise most of the assets transferred. Historically this has resulted in lower transaction costs; e.g., if the annuity provider wants to hold the AIK bonds, these savings can be shared with the plan sponsor through an AIK discount vis a vis the cash price. However, large insurers often have private investing capabilities that have higher expected returns than these bonds. In these situations, PRT annuities are used as sources of long-term capital for the private investing. The higher returns from private investing are used to reduce the PRT price, and AIK discounts are smaller or nonexistent. In fact, in some cases, cash prices now come in lower than AIK prices.

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors.

MetLife Investment Management (MIM), which includes PineBridge Investments, is MetLife Inc.’s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world.

This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

For investors in the U.S.: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities and Exchange Commission (SEC) registered investment adviser. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment adviser.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a "professional client" as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also sub-delegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees' pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being distributed by MetLife Investments Asia Limited (“MIAL”), licensed by the Securities and Futures Commission (“SFC”) for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities in Hong Kong S.A.R. This document is intended for professional investors as defined in the Schedule 1 to the SFO and the Securities and Futures (Professional Investor) Rules only. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are licensed by the SFC to carry on regulated activities in Hong Kong S.A.R. The information contained in this document is for information purposes only and it has not been reviewed by the Securities and Futures Commission.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.