Back in January, we argued that 2026 equity alpha would come from identifying the next beneficiaries of the AI build-out — a thesis that still holds at midyear, though against a more complex backdrop. AI remains the dominant growth engine, and while the market is still highly concentrated, the opportunity set has moved beyond the technology mega-caps as investors look to play the next phase of the AI theme — shifting the focus more toward growth above all and less on resilience and reliable cash flows. Yet geopolitical stress, higher energy prices and uncertainty around the rate path are causing many investors to become more discriminating in how they price risk.

One shift stands out for equity investors: AI adoption is moving from infrastructure build-out toward more visible real-world use, particularly through agentic AI. That matters because it helps explain why capital spending has stayed strong, and why earnings opportunities are broadening across parts of the technology and industrial supply chain. It also draws a harder line between companies with genuine exposure to durable AI demand and those simply riding sentiment. For active investors, that distinction is critical. In our view, the second half of 2026 will be defined by where the market has mispriced the next winners, the overlooked beneficiaries and the businesses still able to compound earnings beyond the narrow leadership driving the indexes.

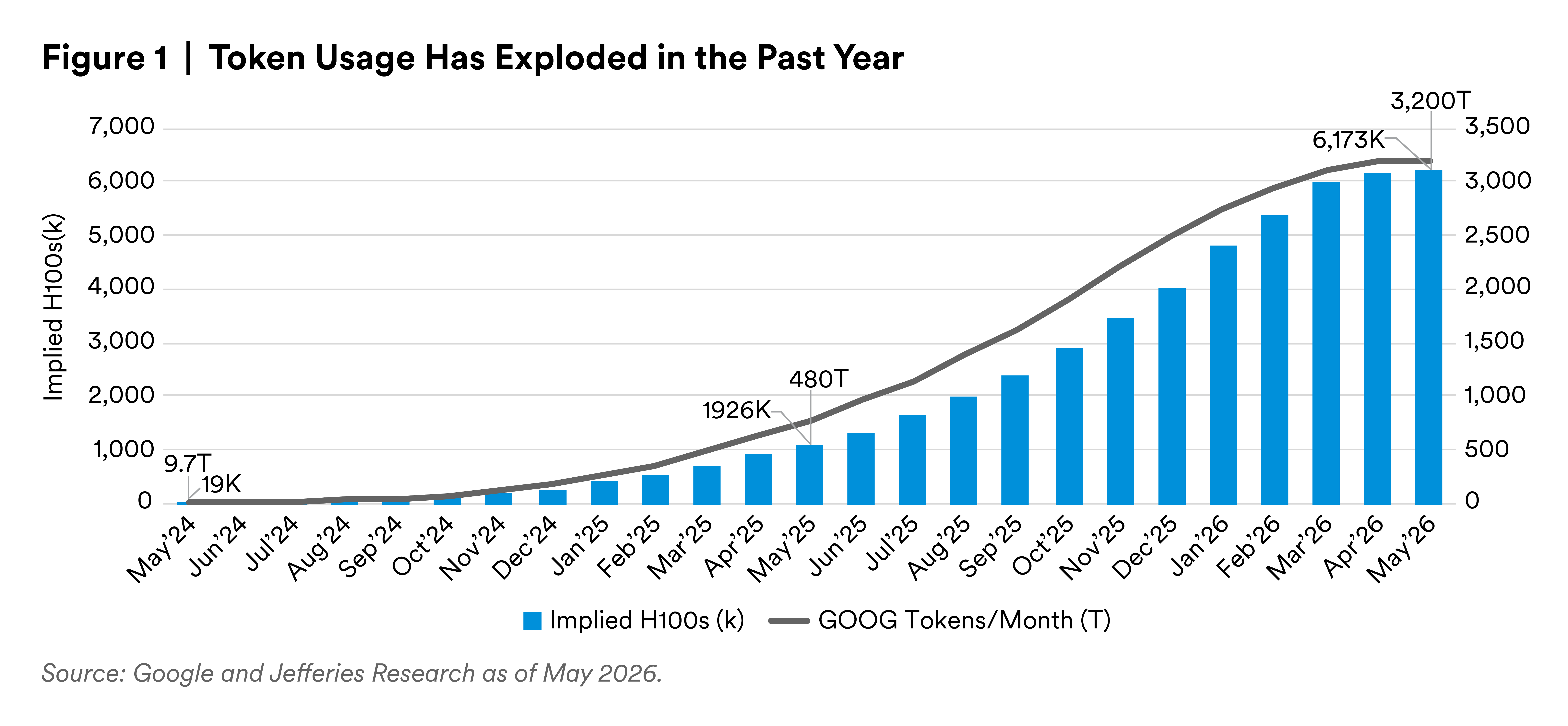

We see the most important development, since early in the year, as the acceleration of AI adoption itself. Earlier phases of the cycle were dominated by model training, infrastructure announcements and debate over whether spending would ultimately be monetized. Following the rapid adoption of agents we began to see toward the end of last year, with leaps in performance from Claude and ChatGPT, the conversation has shifted toward implementation. Agentic AI is moving from promise to practical use — a shift that does not eliminate questions about token efficiency or ultimate returns but does improve visibility into demand. The market is no longer valuing only the possibility of AI; it is increasingly reacting to evidence that spending is translating into usage.

That helps explain why hyperscaler capital expenditures still dominate the corporate investment landscape. Aggregate CapEx looks strong, but much of that strength is still coming from the largest AI spenders. Strip out hyperscalers, and the picture is more subdued. That is both encouraging and cautionary: AI remains the strongest source of incremental growth in the economy, but the broader market is leaning heavily on a relatively small group of companies and themes.

![]()

Even so, the trade is broadening in important ways. The beneficiaries are no longer limited to the obvious large-cap platform and chip names. As AI workloads become more complex and compute-intensive, demand is rippling through memory, logic/foundry, storage, optics, communications equipment, analog semiconductors, power components, semi-cap equipment, specialty materials and so forth. In industrials, companies exposed to data center power generation, electrical equipment, cooling, transmission and related infrastructure have been re-rated higher. Asia and parts of Europe are participating through materials, substrates and supply-chain linkages as well. That is real broadening, but it is not the same as wide market breadth: The opportunity set is widening within the AI ecosystem, while the market itself remains selective.

Indeed, one of the clearest messages we’d give investors is not to confuse broader AI beneficiaries with a genuinely broad market. Leadership has become more concentrated across many parts of the market. A small number of large-cap names still account for an outsized share of returns, while semiconductors occupy an increasingly large weight in the index. In small cap, leadership has also been unusually narrow, centered largely in technology and energy. This concentration can persist longer than many expect, especially while passive flows and benchmark construction continue to reinforce it. But it also creates fragility. If earnings momentum cools, financing costs rise or AI supply-demand imbalances normalize, multiple compression could become a more meaningful headwind.

That concentration risk is one reason we still see a compelling role for active management. Correlations among individual stocks remain quite low, which means bottom-up stock selection opportunities are still abundant, even if benchmark-relative performance is harder to achieve in a market dominated by a handful of mega-cap winners. Investors do not need the whole market to broaden at once for alpha opportunities to emerge. They need dispersion, mispricings and enough fundamental differentiation to reward careful security selection. Today’s market offers all three.

We’re also seeing early signs that the economic backdrop may become more supportive outside the dominant AI complex. ISM and PMI trends are improving after an extended weak stretch, suggesting parts of the economy may be moving into an early-cycle recovery phase. If that improvement broadens, industrial activity could widen beyond the policy-driven and AI-driven pockets that have led so far. Near-shoring and domestic build-out themes remain uneven, but in selected industries, the waiting period may be ending, as companies can no longer defer investment simply because volatility remains high. That is not yet a broadening call, but it argues for watching cyclical businesses whose earnings power could improve if the recovery gains traction.

In the consumer segment, spending has remained surprisingly resilient, but with widening divergence. Higher-income consumers continue to support travel, experiences and premium categories, and even where investors expected a more meaningful slowdown, demand has generally held up better than feared. At the same time, the lower end of the consumer segment is under more visible strain. Credit card and auto defaults are rising, and the burden of accumulated inflation remains heavier for households with less flexibility. The result is an increasingly K-shaped market, with select segments still performing well, while weaker cohorts face mounting pressure.

The Iran conflict adds another variable through higher energy prices. Gas prices are already pressuring some retailers and could become a bigger drag if they stay elevated into the back half of the year. So far, stronger tax refunds and healthy upper-income spending have offset some of the impact. But if energy inflation persists, pressure could spread more broadly through transportation and consumer goods, especially for businesses with limited pricing power. That would raise the stakes in the second half.

Despite these headwinds, we still see attractive opportunities in the consumer sector. With AI beneficiaries monopolizing attention and capital, other segments have become more prone to mispricing. Some consumer companies are beginning to benefit from management changes, restructuring and a renewed focus on execution after several lackluster years. When valuations already reflect skepticism, even modest operational improvement can create attractive upside — exactly the kind of setup where active stock pickers can add value.

Gradual improvement in healthcare has continued, with easing policy-driven headwinds, stabilizing sentiment and firmer demand trends. However, first-quarter earnings mostly showed companies meeting low expectations rather than decisively beating them, leaving investors waiting for cleaner evidence of acceleration. In our view, the recovery story remains credible, but it is not likely to arrive all at once.

Innovation remains the clearest long-term support for the sector. In pharmaceuticals, the outlook for obesity treatments continues to evolve, with oral formulations representing a potentially significant market to unlock, as coverage expands and adoption broadens. New treatments for cardiovascular disease, cancer and autoimmune disease are areas where we are finding investment opportunities. Medical devices and other innovation-driven subsectors also remain constructive. The bottom line is that healthcare innovation is still a powerful opportunity driver, but investors now want a more precise link between product progress, earnings acceleration and valuation support.

Healthcare services continue to face the biggest challenges. In the U.S., ongoing pressure from policy changes is reducing coverage and tightening access through Medicaid and exchange-related channels — a headwind likely to persist unless the political backdrop shifts. For investors, that means the sector does not offer a uniform recovery story. The opportunities are selective, and the pace of improvement will likely vary considerably across subsectors.

Beyond sector fundamentals, the second half of 2026 may hinge on the interaction among energy prices, inflation and monetary policy. If oil stays elevated, cost pressures could increasingly pass through from transportation into core goods and other parts of the economy. That matters for equities because many of the market’s strongest growth areas now depend not only on demand, but also on continued access to capital at tolerable financing costs. If higher inflation leads to a more restrictive Fed stance, or revives the possibility of rate hikes later in the year, companies relying on debt-funded capital spending could face a tougher backdrop.

The market is also looking ahead to potential policy implications from the election cycle, though any major near-term legislative shift appears unlikely if political control remains divided. For now, policy matters more through sector-level effects than through sweeping macro change. Healthcare, energy and regulation-sensitive industries will continue to feel those effects most acutely. Investors should also watch for signs that data center approvals, power availability or supply-chain bottlenecks begin to constrain the AI build-out in more material ways. So far, those issues have not derailed the spending cycle, but they remain important variables to monitor.

Our outlook is constructive but selective. AI remains the defining force in equities, and we believe it is still the most important lens through which to assess market leadership, earnings durability and capital allocation. But the story has matured since January. Adoption is improving. Beneficiaries are broadening across the supply chain. Concentration risks are building. And outside the AI complex, opportunities are emerging where misplaced skepticism, successful restructuring or gradual cyclical improvements have left valuations more compelling than the headlines suggest.

For the rest of 2026, we believe the best alpha opportunities are likely to come from disciplined stock selection rather than a simple call on market direction. Investors should focus on companies with tangible earnings support, differentiated exposure to enduring themes and enough balance-sheet and pricing flexibility to navigate higher energy costs, policy noise and an uncertain rate backdrop.

In a market where the index looks narrow and the headlines are dominated by a handful of names, the case for active investing is not weaker. If anything, it is stronger.

Disclosure

MetLife Investment Management ("MIM"), which includes PineBridge Investments, is MetLife, Inc.'s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world. The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risk, including possible loss of principal; no guarantee is made that investments will be profitable. This document is solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. Views may be based on third-party data that has not been independently verified. MIM does not approve of or endorse any republication of this material. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results.

For investors in the U.S.: This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities and Exchange Commission (SEC) registered investment adviser. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment adviser.

For investors in the UK: This document is being distributed by MetLife Investment Management Limited (“MIML”), authorised and regulated by the UK Financial Conduct Authority (FCA reference number 623761), registered address One Angel Lane 8th Floor London EC4R 3AB United Kingdom. This document is approved by MIML as a financial promotion for distribution in the UK. This document is only intended for, and may only be distributed to, investors in the UK who qualify as a “professional client” as defined under the Markets in Financial Instruments Directive (2014/65/EU), as per the retained EU law version of the same in the UK.

For investors in the Middle East: This document is directed at and intended for institutional investors (as such term is defined in the various jurisdictions) only. The recipient of this document acknowledges that (1) no regulator or governmental authority in the Gulf Cooperation Council (“GCC”) or the Middle East has reviewed or approved this document or the substance contained within it, (2) this document is not for general circulation in the GCC or the Middle East and is provided on a confidential basis to the addressee only, (3) MetLife Investment Management is not licensed or regulated by any regulatory or governmental authority in the Middle East or the GCC, and (4) this document does not constitute or form part of any investment advice or solicitation of investment products in the GCC or Middle East or in any jurisdiction in which the provision of investment advice or any solicitation would be unlawful under the securities laws of such jurisdiction (and this document is therefore not construed as such).

For investors in Japan: This document is being distributed by MetLife Investment Management Japan, Ltd. (“MIM JAPAN”), a registered Financial Instruments Business Operator (“FIBO”) conducting Investment Advisory Business, Investment Management Business and Type II Financial Instruments Business under the registration entry “Director General of the Kanto Local Finance Bureau (Financial Instruments Business Operator) No. 2414” pursuant to the Financial Instruments and Exchange Act of Japan (“FIEA”), and a regular member of the Japan Investment Advisers Association and the Type II Financial Instruments Firms Association of Japan. In its capacity as a discretionary investment manager registered under the FIEA, MIM JAPAN provides investment management services and also sub-delegates a part of its investment management authority to other foreign investment management entities within MIM in accordance with the FIEA. This document is only being provided to investors who are general employees’ pension fund based in Japan, business owners who implement defined benefit corporate pension, etc. and Qualified Institutional Investors domiciled in Japan. It is the responsibility of each prospective investor to satisfy themselves as to full compliance with the applicable laws and regulations of any relevant territory, including obtaining any requisite governmental or other consent and observing any other formality presented in such territory. As fees to be borne by investors vary depending upon circumstances such as products, services, investment period and market conditions, the total amount nor the calculation methods cannot be disclosed in advance. All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Investors should obtain and read the prospectus and/or document set forth in Article 37-3 of Financial Instruments and Exchange Act carefully before making the investments.

For Investors in Hong Kong S.A.R.: This document is being distributed by MetLife Investments Asia Limited (“MIAL”), licensed by the Securities and Futures Commission (“SFC”) for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 9 (asset management) regulated activities in Hong Kong S.A.R. This document is intended for professional investors as defined in the Schedule 1 to the SFO and the Securities and Futures (Professional Investor) Rules only. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are licensed by the SFC to carry on regulated activities in Hong Kong S.A.R. The information contained in this document is for information purposes only and it has not been reviewed by the Securities and Futures Commission.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

For investors in the EEA: This document is being distributed by MetLife Investment Management Europe Limited (“MIMEL”), authorised and regulated by the Central Bank of Ireland (registered number: C451684), registered address 20 on Hatch, Lower Hatch Street, Dublin 2, Ireland. This document is approved by MIMEL as marketing communications for the purposes of the EU Directive 2014/65/EU on markets in financial instruments (“MiFID II”). Where MIMEL does not have an applicable cross-border licence, this document is only intended for, and may only be distributed on request to, investors in the EEA who qualify as a “professional client” as defined under MiFID II, as implemented in the relevant EEA jurisdiction. The investment strategies described herein are directly managed by delegate investment manager affiliates of MIMEL. Unless otherwise stated, none of the authors of this article, interviewees or referenced individuals are directly contracted with MIMEL or are regulated in Ireland. Unless otherwise stated, any industry awards referenced herein relate to the awards of affiliates of MIMEL and not to awards of MIMEL.